INDEX

In Japan, disclosure of sustainability information is mandatory in securities reports and other reports after March 31, 2023.

The SASB Standard, proposed by the SASB (U.S. Sustainability Accounting Standards Board) as an international framework (standard for disclosure requirements) for sustainability information disclosure, is a standard that is gaining international recognition, and the number of companies adopting it is increasing, regardless of country or region.

The SASB Standards stipulate ESG information disclosure for each of the 11 industries and 77 business sectors that are primarily targeted at investors. By ensuring fair disclosure of information among companies, the SASB Standards not only provide investors and evaluation criteria for deciding which companies to invest in, but are also expected to have a significant effect in hedging risks and improving branding in corporate management.

In the past, aiESG has published two articles on the SASB Standards, one before and one after, summarizing the benefits of adopting the SASB Standards and the detailed disclosure requirements.

What is the SASB Standard for ESG Information Disclosure? (Part 1)Outline of SASB

What is the SASB Standard for ESG Disclosure? (Part 2) Benefits for Companies

This report summarizes the latest information on the state of adoption of the SASB Standards by Japanese companies for those in charge who are considering adopting the SASB Standards within their own companies. In addition, aiESG is the first ESG evaluation organization in Japan to be licensed under the SASB Standards, the international sustainability standard. In addition to the latest information, this report also discusses aiESG's services for report preparation.

1. international status of SASB standards

The SASB Standards have been proposed internationally to ensure the visibility of information when companies release sustainability disclosure reports (e.g., integrated reports). The SASB Standards set standards for non-financial disclosures.

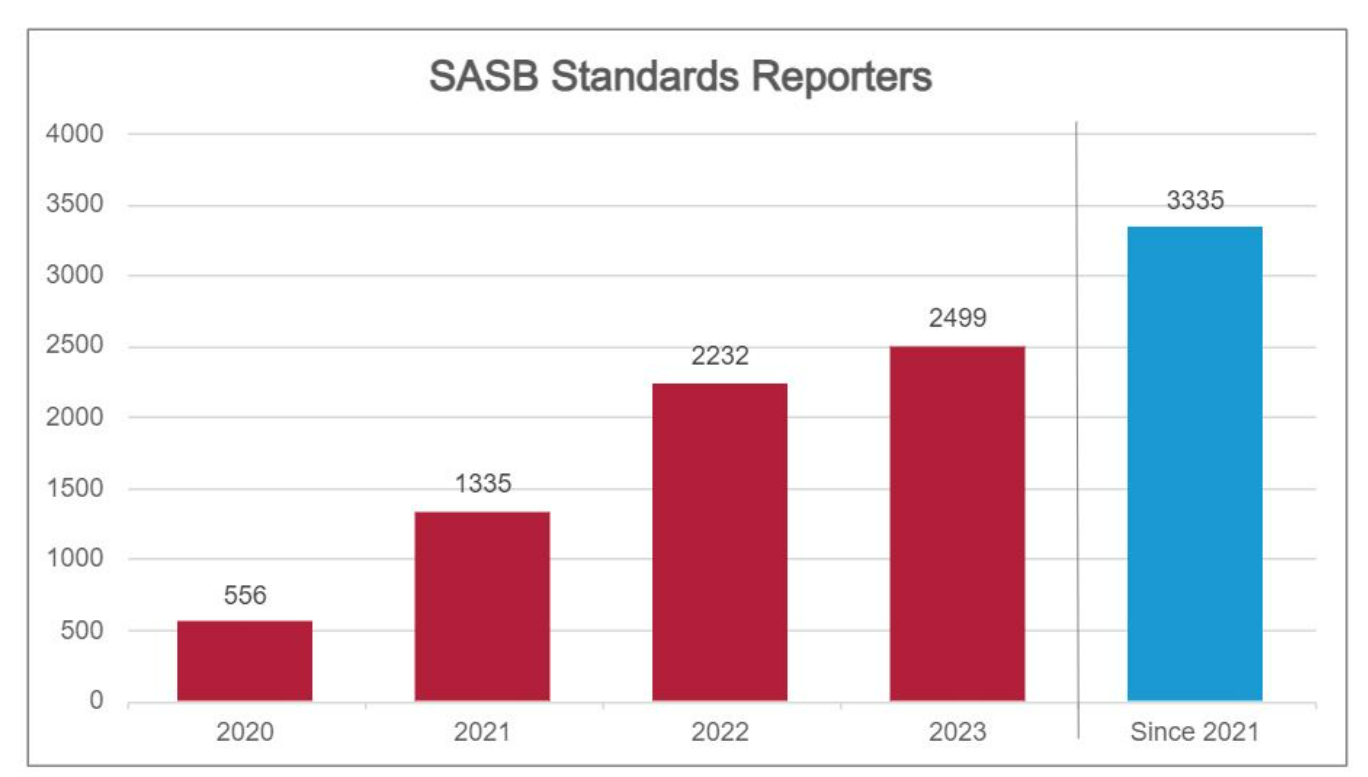

As shown in Figure 1, since the SASB Standards were proposed, an increasing number of companies, both national and regional, have adopted the SASB Standards in their sustainability information reports. Of the companies in the S&P Global 1200 Index that provide effective exposure to global equity markets, 906 have adopted the SASB Standards in their sustainability reports (cumulative total since 2021).

Figure 1: Number of companies that have prepared a SASB Standard Report (red graph: number of companies by year; blue graph: cumulative number of companies since 2021) -. SASB WebsiteAdapted from

Although the SASB standards are not legally binding, an increasing number of companies are adopting them because non-financial information disclosed in accordance with the standards has significant price informativeness [1].

Price informativeness indicates the degree of information and value contained in the asset price. This means that the information disclosed has financial relevance to investors. This means that disclosure in accordance with SASB standards is advantageous to investors as they can determine whether the actual stock price corresponds to the price of the stock according to the publicly available information.

In addition, price informativeness has been shown to work strongly with companies that have a large number of investors who are interested in sustainability, so the SASB standard is expected to become important in a commercial environment where international awareness of sustainability is increasing.

Figure 2: Companies adopting SASB standards, classified by sector (cumulative number of companies from 2020 to 2023):. SASB Websitesee

As Figure 2 shows, although the number of companies adopting the SASB standard may be small or large, it can be confirmed that all sectors (industries are further classified from here) are supported by companies adopting the SASB standard.

As SASB becomes more widespread, Japanese companies will increasingly consider adopting the SASB standards for their sustainability reports in order to provide transparent information to investors.

As an actual case study, we will review examples of employment by Japanese companies in the next section.

2. adoption of SASB by domestic companies

An increasing number of Japanese companies are adopting the SASB standards for their own sustainability information reporting.Official SiteThe total number of companies that have adopted the SASB standard published above is 84 since 2020.

Many Japanese companies are complying with the SASB Standards by adding a separate section at the end of their reports (e.g., Sustainability Report, Integrated Report, etc.), such as a "SASB Index Response Table.

This report introduces the form of the SASB report after selecting five Japanese companies that have included SASB Standard compliance in their 2023 reports.

| Company Name | sector | industry | report format |

| Asahi Kasei | resource transformation | Chemical | Sustainability Report |

| Kyushu Electric Power Co. | infrastructure | Electric Utilities & Power Generators | Integrated Report |

| Mazda | transportation | Automobiles | SASB Indicators Report |

| Nissui | Food & Beverage | Processed FoodMeat,Poultry & Dairy | Sustainability Report |

| Takeda Pharmaceutical Company Limited | health care | Biotechnology & Pharmaceuticals | SASB Indicators Report |

Table 1: Firms that Complied with the SASB Standard in 2023 (prepared by the authors)

All of the five companies mentioned above have prepared their reports in a manner that matches their non-financial information with the disclosure requirements specified by the SASB Standards. In addition, as Nissui illustrates, it is possible to combine information from multiple industries in the same report, confirming that the SASB Standards are sustainability standards that enable flexible and concise presentation of information.

The following two formats can be used to demonstrate compliance with the SASB standard.

1. utilize corresponding hyperlinks in the report to pages that describe the designation requirements.

(Asahi Kasei, Mazda, Nissui)

2. a table showing the specified requirements and their responses on the same page. (Kyushu Electric Power, Takeda Pharmaceuticals)

Both formats are able to report according to SASB standards in both cases, which is an important indicator for investor decisions.

The report published by Asahi Kasei includes notes on the calculation method of greenhouse gas emissions specified in the SASB Standard, and other information on the process of indicator publication.

The SASB also noted that the Kyushu Electric Power Company and Takeda reports are highly commendable in that they provide detailed rationale for not disclosing the indicators, suggesting that while there is no obligation to address all of the requirements, it would have a positive impact on investors to include the reasons when they cannot be addressed.

Thus, complying with the SASB Standards is synonymous with clarifying the relevance of the requirements specified by the SASB side to the disclosure of non-financial information disclosed (maintained) by the company.

However, there are many examples of companies that do not try to meet all of the requirements, such as the companies mentioned above, and many companies disclose information about some of the requirements, or otherwise only make limited efforts to comply with the SASB Standards.

This is also an advantage because the SASB Standards are not mandatory, meaning that companies can take steps to find the relevance of their public information to the SASB Standards.

3. aiESG's services for compliance with SASB standards

The SASB Standard is divided into "quantitative indicators" and "qualitative indicators (discussion)" regardless of industry.

Qualitative indicators are often asked about medium- and long-term strategies on the part of the company, and it is expected that they can be addressed through coordination with the company's own management plan.

On the other hand, it is confirmed that indicators such as "greenhouse gas emissions in the supply chain" are a major barrier to compliance with the SASB standard, as they cannot be calculated using only the information held within the company.

One of aiESG's major strengths is its ability to calculate quantitative indicators with our proprietary big data, using basic transaction information possessed by the company. The indicators that can be calculated include not only "greenhouse gas" but also "wastewater treatment" and "potential for forced labor," covering both environmental and social aspects.

If you are a corporate representative considering the calculation of quantitative indicators when complying with the SASB standards, please contact aiESG.

Contact us:

https://aiesg.co.jp/contact/

(Reference)

1: Grewal, J., Hauptmann, C. & Serafeim, G. Material Sustainability Information and Stock Price Informativeness. J Bus Ethics171, 513-544 (2021). https://doi.org/10.1007/s10551-020-04451-2

*Related Article*.

Report List : Regulations/Standards

https://aiesg.co.jp/topics/report/tag/基準-規制/

What is the SASB Standard for ESG Information Disclosure? (Part 1)Outline of SASB

https://aiesg.co.jp/topics/report/2301025_sasb1/

What is the SASB Standard for ESG Disclosure? (Part 2) Benefits for Companies

https://aiesg.co.jp/topics/report/2301115_sasb2/

Commentary] Alphabet Soup: The Disruptions and Convergence of Sustainability Standards

https://aiesg.co.jp/topics/report/2301226_alphabet-soup/

Commentary] Non-Financial Capital: Trends in Human and Natural Capital -Disclosure Regulations and Guidelines in Japan and Overseas

https://aiesg.co.jp/topics/report/240329_human-natural-capital/