INDEX

Social Aspects of Nonfinancial Information Disclosure

Frameworks for ESG information disclosure, such as TCFD, TNFD, and SASB, have been continuously updated in recent years, and companies need to consider a variety of disclosures that are in line with the reality of their business and the demands of society.

This article introduces the successive and latest frameworks and the responses required of companies to the growing social aspects of risk and concern, which are gaining increasing attention following climate change and environmental issues.

Importance of the Social Sector in ESG

Of the three components of ESG - Environment, Social, and Governance - the environmental area has been the most frequently discussed. In fact, the Task Force on Climate-related Financial Disclosures (TCFD) and the Task Force on Nature-related Financial Disclosures (TNFD) have been the focus of much attention. (Taskforce on Climate-related Financial Disclosures) and TNFD (Taskforce on Nature-related Financial Disclosures) have all focused on environmental issues.

However, social issues such as human rights and inequality are similar to environmental issues in that they are also major themes that must be addressed by the international community as a whole. These issues, which have historically persisted, are now attracting renewed attention, and not only the efforts of the United Nations and national governments, but also the policies and approaches of companies are beginning to be questioned.

Social Sector Issues and Corporate Responsibility

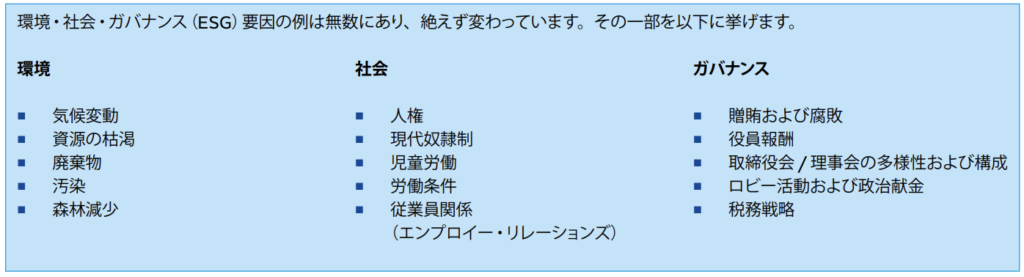

The United Nations Principles for Responsible Investment (PRI) lists human rights, modern slavery, child labor, working conditions, and employee relations as examples of ESG social factors (Figure 1).

Figure 1: Examples of ESG factors (Source:Principles for Responsible Investment (PRI))

In the past, major issues such as regional disparities and child labor were considered to be issues that should be addressed by the international community and national governments, while issues for which companies were responsible were mainly those that occurred within their own companies, such as discrimination against women and harassment. However, the social issues presented by PRIs are not only internal to companies, but also include labor environment and inequality issues that can be traced back to the entire supply chain. the trend of ESG investment requires companies to understand the mutual impacts and risks of these issues to their own companies and disclose this information to consumers and investors.

Human Rights and Inequality Related Framework

The history of international frameworks related to social issues is long, and various human rights and inequality-related frameworks have been proposed. The following table summarizes the guidelines that are particularly relevant to business and their relationship to companies and organizations.

Table 1: Human Rights and Inequality-Related Framework (Prepared by Author)

| Name (Organization,Year of Publication) | summary | Utilization and participation of companies |

| OECD Guidelines for Multinational Enterprises (OECD, 1976) | Guidelines for recommending that companies voluntarily take the responsible actions expected of them Revised 2023 | Voluntary use] Not legally binding. |

| SA8000 (SAI, 1997) | International standards for the exercise of all employee rights and the protection of employees 4th edition in 2014. | Certification and Participation Third-party audit required for acquisition ⇒ Audit every six months |

| ILO Core Labour Standards (ILO, 1998) | Ten conventions in five areas of fundamental principles and rights at work (minimum standards to be observed) Safe and healthy working environment" added in June 2022 | Other Obligations to Member States |

| Ten Principles of the Global Compact (UNGC, 2000) | Ten principles in four areas (human rights, labor, environment, and anti-corruption) adopted and agreed upon globally | Certification and Participation Signature ⇒ Reporting obligation |

| ISO 26000 (ISO, 2010) | International Standard for Social Responsibility of Organizations | Voluntary Use Not a certified standard |

| Guiding Principles on Business and Human Rights (United Nations, 2011) | Global standards to be respected by all countries and companies National Action Plan (NAP) | Voluntary Use Not legally binding, but compliance is encouraged by the NAP |

| UN Guiding Principles Reporting Framework (United Nations, 2015) | First comprehensive guidance for companies to report on human rights issues in accordance with the above Guiding Principles Japanese version in 2017 | Report] Statement of minimum standards and use of framework |

| Action Plan on Business and Human Rights (2020-2025) (Japan, 2020) | Japanese NAP of the Guiding Principles on Business and Human Rights Expectations of various government policies and companies | Voluntary Use Formulation of human rights policy, implementation of human rights DD, and establishment of remedy mechanisms are expected. |

| Handbook for Management Respecting Human Rights (Keidanren, 2021) | Guidance on disseminating the UN Guiding Principles and providing guidance on human rights DD and specific examples of human rights issues in the international community. | Voluntary Use Encouraging member companies to strengthen their efforts Cautious about mandates |

| Guidelines for Respecting Human Rights in Responsible Supply Chains, etc. (Japan, 2022) | Guidelines to promote respect for human rights by companies based on international standards Based on the UN Guiding Principles, OECD Guidelines for Multinational Enterprises, and ILO Declaration on Multinational Enterprises | Voluntary Use Not legally binding. Can refer to specific steps for implementation of human rights DD |

| Tackling inequality:Guidelines for Corporate Behavior (BCTI, 2023) | Report by the Business Committee to Tackle Inequality (BCTI), established by the WBCSD 10 actions companies can take to address inequality | Voluntary Use |

| TISFD[1] (TISFD, 2024 or later) | Framework for Financial Disclosure on Social and Inequality-Related Issues | Report] Disclosure in line with the framework |

The Guiding Principles on Business and Human Rights adopted by the United Nations in 2011 clarified that companies have a responsibility to respect human rights. Since then, "human rights due diligence (human rights DD)," in which companies investigate and curb the risk of human rights violations related to their business activities, has been recognized and spread worldwide. In particular, since the "UN Guiding Principles Reporting Framework" in accordance with the above-mentioned Guiding Principles was formulated in 2015, there has been a trend toward mandatory human rights DD, especially in Europe [2]. In Japan, there is no legally binding framework yet, but companies are being encouraged to take action through action plans and guidelines, and companies that provide services in the EU are already being affected by the mandate.

However, at present, many frameworks only provide principles and guidelines, and the approach for each company to actually investigate and disclose information is not yet sufficiently widespread. Guidelines that provide specific guidance are being formulated in parallel by various organizations both in Japan and overseas. Companies that are considering strengthening disclosure of social aspects in the future must start by carefully examining which standards they should follow in conducting risk surveys[3], which may ultimately lead to raising the hurdle for information disclosure.

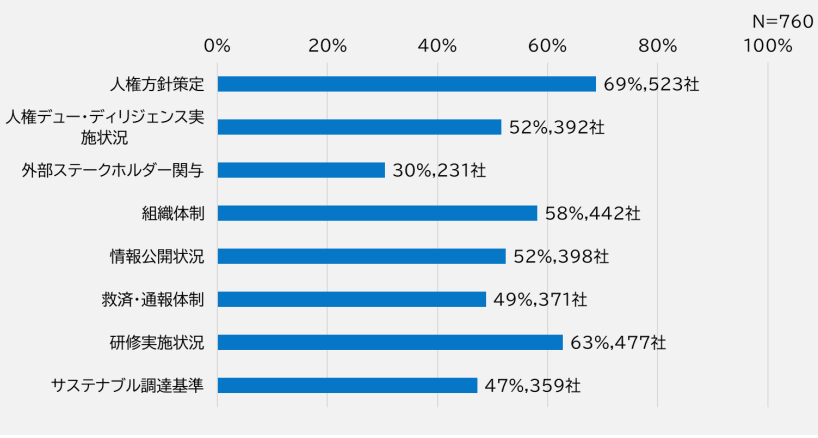

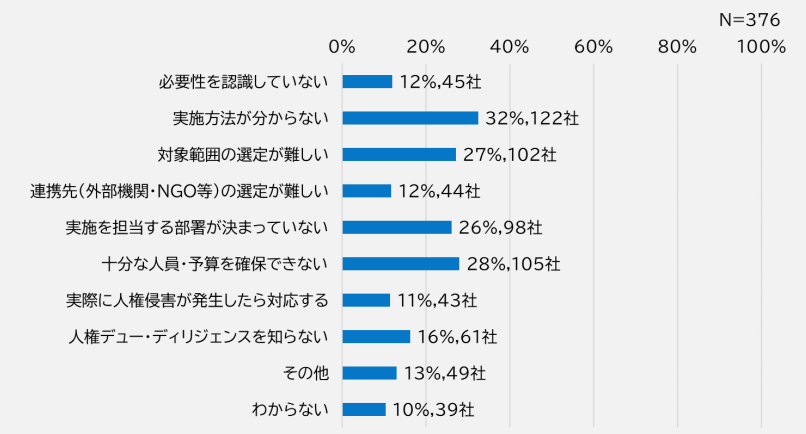

According to a survey conducted by the Japanese government in 2021, 52% of companies have implemented human rights DD, and around 30% of those that have not reported difficulties in selecting the method and scope of implementation (Figures 2 and 3).

Figure 2: Status of Corporate Initiatives on Human Rights

(Source:Results of the "Questionnaire Survey on the Status of Human Rights Initiatives in the Supply Chains of Japanese Companies)

Figure 3: Reasons for not implementing human rights DD

(Source:Results of the "Questionnaire Survey on the Status of Human Rights Initiatives in the Supply Chains of Japanese Companies)

Benefits and Processes for Companies to Address Human Rights DD

While the growing international concern for human rights and inequality is putting pressure on individual companies to address human rights DD, it is also in the company's own interest to properly disclose social aspects of its operations.

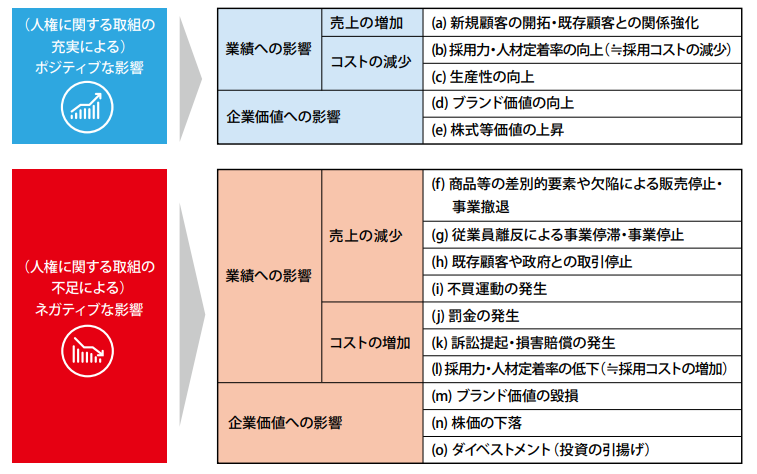

The "Research and Study on Business and Human Rights" report[4] prepared by the Ministry of Justice in 2021 summarizes the impact of human rights initiatives on business activities, both positive and negative (Figure 4).

Figure 4: Impact of Human Rights Initiatives on Business Activities

(Source:Report on "Research and Study on Business and Human Rights)

Neglecting human rights issues related to business activities can lead to problems that directly damage corporate management, such as reduced productivity and mass turnover, in addition to risks similar to those in other areas of ESG, such as deterioration of corporate image and stock price.

So what steps do companies actually need to take when addressing human rights DD? According to the "Guidelines for Respecting Human Rights in Responsible Supply Chains, etc." published by the Japanese government[5], the first step is to identify and assess the negative human rights impacts that a company's business activities may involve. The process involves the following

1. identify business areas of significant risk

Identify business areas where risk is considered significant, considering factors such as type of risk and regional characteristics.

2. identification of the process of occurrence of negative impacts

Specify how negative impacts will occur in each process of the project.

3. assessment of negative impacts and corporate involvement

Evaluate whether the entity caused the negative impact, contributed to the negative impact, and whether the negative impact is directly related to the entity.

4. prioritization

We will deal with the most serious and probable cases first.

Once priorities are determined, various measures are considered to prevent or mitigate those negative impacts. These measures vary depending on the industry and the scale of the business, but may include improving relationships with specific suppliers or suspending business with them. The human rights DD process also includes evaluation of the effectiveness of the measures taken, as well as internal and external explanation and information disclosure.

For many companies, identifying and assessing where and how their products and services relate to human rights risks can be challenging.

The services provided by aiESG enable ESG analysis not only on a company or business unit basis, but also on a product or service basis. In addition to indicators such as greenhouse gas emissions, which can be measured by conventional services, aiESG can also quantify various factors related to human rights, such as community impact and indigenous rights Furthermore, for each item, it is possible to identify hotspots of high risk areas in the supply chain, leading to the identification of high-risk regions and business areas.

Conclusion

In this article, we have introduced the importance of social risks among the three ESG factors and the trends in Japan and abroad. As each company is required to disclose information not only within the company but also about the entire supply chain, it is important to first identify, to the extent possible, where the company's social risks lie.

To date, ESG information disclosure has been based on international frameworks such as the environment-related TCFD and nature-related TNFD, which have shown effective and comprehensive disclosure methods. The Task Force on Inequality and Social-related Financial Disclosures (TISFD), which will begin full-scale activities after 2024, is currently attracting attention as a social and inequality-related framework to follow these frameworks. Task Force on Inequality and Social-related Financial Disclosures (TISFD). We will be posting more information about TISFD on this website in the near future.

aiESG can assist you with everything from the basics of the TISFD and related frameworks to the actual disclosure of non-financial information, so please contact us if you need help with the social aspects of ESG disclosure.

Contact us:

https://aiesg.co.jp/contact/

Bibliography

[1] A new disclosure framework following TCFD and TNFD (to be explained in detail in the next blog). The name is tentative and may change in the future (seeTaskforce on Inequality and Social-related Financial Disclosures (TISFD) | Groups | LinkedIn)

[2] https://www.ilo.org/tokyo/information/terminology/WCMS_791223/lang–ja/index.htm

[3] https://www.meti.go.jp/press/2021/11/20211130001/20211130001-1.pdf

[4] ff71991849952a56349b71abb955b8e61fa549fe.pdf (jinken-library.jp)

[5] 20220913003-a.pdf (meti.go.jp)

Related page

Report List : Regulations/Standards

https://aiesg.co.jp/topics/report/tag/基準-規制/

[Paper description] The Impact of Climate Change on Conflict: A Systematic Review of the Vulnerability Conditions of Societies.

https://aiesg.co.jp/topics/report/report_climatechange_conflict/

[Commentary] Nikkei article: aiESG Supply Chain Analysis of "Electric Vehicle (EV) Production, ESG Indicators Deteriorate Due to 'De-China'".

https://aiesg.co.jp/topics/report/2301016_nikkeiev1/

【【Explanation] What is TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/topics/report/230913_tnfdreport/

What is the SASB Standard for ESG Information Disclosure? (Part 1)Outline of SASB

https://aiesg.co.jp/topics/report/2301025_sasb1/

CSRD: The EU Sustainability Reporting Standard Just Before It Enters into Force: The Impact on Japanese Companies

https://aiesg.co.jp/topics/report/2301120_csrd/