INDEX

1. Introduction

The "Paris Agreement" was adopted at the 21st Conference of the Parties (COP21) to the United Nations Framework Convention on Climate Change in 2015.

The Paris Agreement, covering all countries and regions, agreed to limit the global average temperature increase from pre-industrial times to well below 2°C, and if possible to 1.5°C. In 2021, the Glasgow Climate Accord at COP26 set a common global goal to limit the increase to 1.5°C. The Paris Agreement is the first time that a climate change agreement has been reached in the world.

Meanwhile, on June 5, 2024, the World Meteorological Organization (WMO) released a report analyzing the outlook for climate change up to five years from now, which indicated that the average temperature for the entire five-year period from 2024 to 2028 is likely to increase by more than 1.5°C above pre-industrial levels at 471 TP3T, up from last year's The report noted that this is up from 32% indicated by the report [1].

As UN Secretary-General Guterres made a scathing appeal for efforts to curb global warming on the same day[2], there are calls from investors, corporations, NGOs, and others for stricter and faster global warming measures.

In recent years, not only GHG but also ESG and sustainability have been attracting attention, and comprehensive information disclosure that goes beyond climate change is required. In line with this trend, organizations supporting ESG measurement, disclosure, and reporting are emerging one after another.

This paper describes the importance of the shift to ESG, touching on organizations working to reduce greenhouse gas (GHG) emissions and their specific metrics and targets.

2. examples of specific institutions and indicators

This chapter introduces the organizations and indicators involved in GHG measurement, disclosure, and reporting, and discusses the latest trends. Figure 1 shows examples of organizations involved in GHG reduction, with different roles depending on the size of the sector. This text introduces a selection of some of them.

Figure 1: Examples of indicators and institutions involved in GHG reduction

◆IPCC (Intergovernmental Panel on Climate Change)

The IPCC is a United Nations agency established in 1988 by the World Meteorological Organization (WMO) and the United Nations Environment Programme (UNEP). It currently has 195 member countries and provides governments with scientific information that can be used to formulate climate policies.

Assessment reports published by the IPCC are an important source of information in international climate change negotiations because they summarize the drivers of climate change, their impacts and future risks, and the risks of mitigating them, based on assessments of numerous papers by experts.

Published by IPCCguidelineare encouraged to be referenced in the preparation of the Greenhouse Gas Inventory, which the United Nations Framework Convention on Climate Change requires developed countries to submit annually.

*Greenhouse gas inventory: A document that summarizes and documents the emission and absorption volumes and calculation methods of each country.

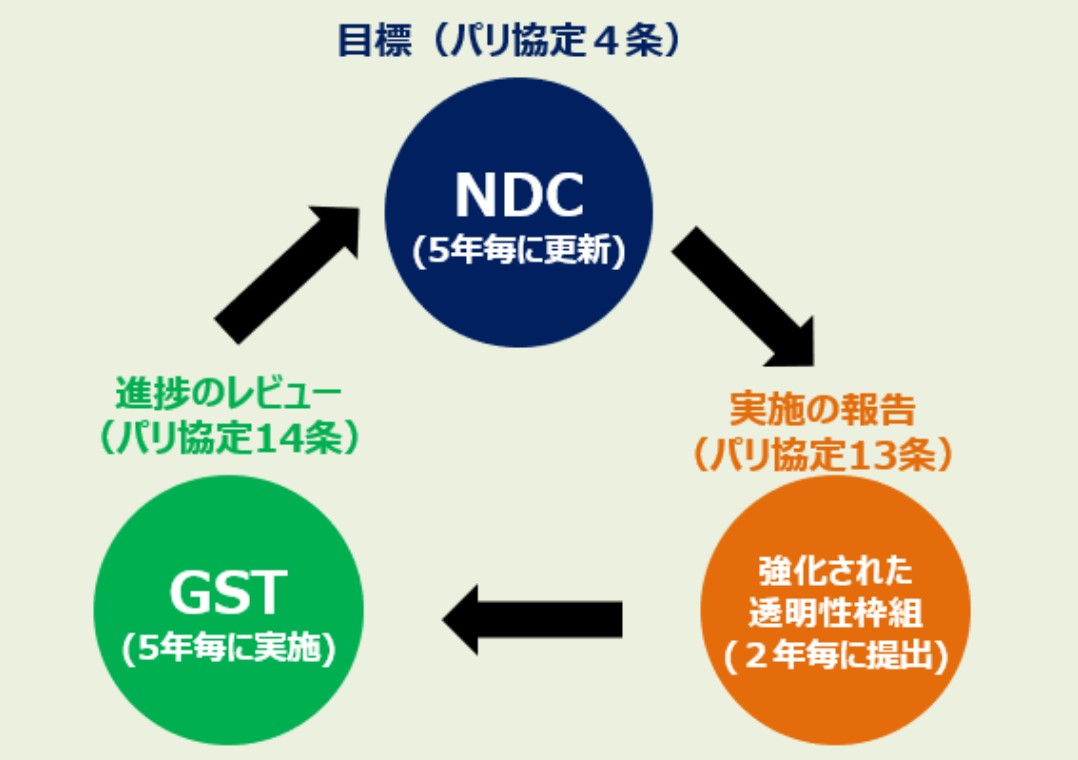

◆Global Stocktake:(GST)

At COP28 in 2023, the Global Stocktake (GST) was conducted for the first time since the entry into force of the Paris Agreement to assess the progress of the entire world toward achieving the goals set forth in the Paris Agreement.

Every five years, the GST assesses the progress of the world as a whole in achieving the goals of the Paris Agreement and provides recommendations for action to be taken by each country. Each country then updates its own greenhouse gas emission reduction targets (NDC) based on the results of the GST. Furthermore, each country is required to implement measures toward the NDC it has established and submit a report every two years.

In this way, we aim to steadily achieve the goals of the Paris Agreement by repeating the cycle in which each country formulates its NDC based on the GST, reports on the implementation of the NDC, and uses the results in the next GST.

Figure 2: Position of Global Stocktaking in the Paris Agreement(in Japanese history)Agency for Natural Resources and Energy, Ministry of Economy, Trade and Industry HP(Adapted from.)

◆SBTi (Science Based Targets Initiative)

SBTi (Science Based Targets Initiative) is a joint initiative established by WWF and CDP in 2015 with the aim of preventing climate change and increasing the competitiveness of companies in a net-zero economy.SBTi is creating SBTs ( Science-based Targets) are common science-based GHG emission reduction targets, and participating companies are required to set their SBTs based on guidance developed by SBTi.

Compliant companies are given SBT certification and are required to report and disclose their emissions and progress on measures on an annual basis. They are then required to periodically check the adequacy of their targets and re-set them if any major changes occur. Doing so will lead to recognition from investors and consumers, as well as enable the company to respond to requests for disclosure of GHG reduction targets from companies in its own supply chain.

As of August 19, 2024, 8759 companies worldwide and more than 1,200 Japanese companies have joined the SBTi, which has now become the international de facto standard and one of the most important indicators for GHG emission reductions.

On February 28, 2024, two reports were published on Beyond Value Chain Mitigation (BVCM), which refers to the reduction of carbon emissions across the value chain. The BVCM has been organized in such a way that it is now possible to set even clearer climate targets [3], as the criteria for BVCM had been unclear until now.

◆SBTN (Science Based Targets Network)

SBTN (Science Based Targets Network) is an initiative established in 2019 by CDP and the World Resources Institute (WRI), and can be positioned as a complement to SBTi.

The aforementioned SBTi.climateThe SBTN focuses on climate, but also on biodiversity and environmental impacts across land, freshwater, and marine environments.comprehensiveWe are working on the SBTs for Nature, a science-based guidance for companies and cities to set nature-related goals that go beyond climate change, and is working to expand its reach to more companies and cities.

A plan to set SBTs for Nature for cities was presented at COP28 in 2023; the first guidance is expected to be operational starting in 2025.

Please refer to the following article for more information on SBTs for Nature.

Description] SBTs for Nature - science-based nature-related goals

◆GHG Protocol

The GHG Protocol is an internationally recognized GHG emissions accounting and reportingDeveloping standardsThe purpose of this program is to promote the use of the system.

The Corporate Standards published by the GHG Protocol are intended for companies to measure their emissions from electricity and other energy purchases and have been used by companies around the world since their release in 2001. 2011 saw the release of the Scope 3 Metrics, which remain influential as the only internationally recognized standard for Scope 3. In 2011, the Scope 3 standard was published and remains influential as the only internationally recognized standard for Scope 3.

In recent years, the "FLAG" (forest, land, and agriculture sector) has also received a lot of attention, and new guidance is expected to be issued in the first quarter of 2025 to account for emissions from that sector. [4]

◆ISO 14064/14065ISO

ISO (International Organization for Standardization) is an NGO whose purpose is to establish internationally accepted plans.

ISO 14064/14065 provides a framework for uniform GHG accounting rules, verification rules, and requirements for verification bodies. ISO 14064 is further divided into three parts, with different rules for different processes in GHG accounting. ISO 14065 sets forth requirements for verification bodies.

Table 1: Rules defined by ISO 14064/14065(in Japanese history)Ministry of the Environment(Prepared by the author based on)

| ISO 14064-1 | Rules for GHG calculation in organizations (companies, factories, etc.) |

| ISO 14064-2 | Rules for Calculating Project Emission Reductions and Absorptions |

| ISO 14064-3 | Rules for validation and verification of GHG calculations |

| ISO 14065 | Sets forth the requirements for verification bodies. |

The GHG Protocol does not include a comprehensive nature-related standard, as many of the GHG-related items are common to the GHG Protocol.

◆CDP(in Japanese history)Carbon Disclosure Project) Japan

CDP is a non-governmental organization (NGO) of British origin that operates a global disclosure system to help investors, companies, nations, and others manage their environmental impacts.CDP Home Page(from).

CDP sends the "CDP Questionnaire" to companies and scores them on environmental risks and opportunities based on their responses. The questionnaire includes questions related to GHG emissions and allows companies to measure GHG emissions in a variety of ways, including aggregating data by location for large companies; it is aligned with frameworks and standards such as IFRS S2 and TNFD, and helps companies interoperate with multiple frameworks.

On November 1, 2023, CDP also requested that more than 2,100 companies worldwide with high CO2 emissions establish SBTs. The total Scope 1 and 2 emissions of the targeted companies amounted to 8.3 Gt, which is equivalent to the national emissions of the U.S., Japan, and the U.K. The total market capitalization of the targeted companies was approximately US$28 trillion (approximately $44.4 trillion). The total market capitalization of the companies involved is approximately US$28 trillion (approximately 440 trillion yen). The request has been endorsed by 307 institutional investors and financial institutions and 60 global companies [5].

Shift to ESG - Toward Comprehensive Sustainability Information Disclosure

While the previous section has focused on indicators and organizations related to GHG emissions, in recent years, the importance of comprehensive sustainability information disclosure has increased beyond GHG emissions. (PRI) in 2006, ESG (Environmental, Social, and Corporate Governance) has become more important in achieving a sustainable society.

The most representative examples of the GHG to ESG shift are the TCFD and TNFD The Task Force on Climate-related Financial Disclosures (TCFD), established in 2015, has been working on four The TCFD has been recommending climate change-related disclosures in terms of governance, strategy, risk management, and indicators and targets.

In recent years, however, it has become clear that nature and ecosystems, including biodiversity as well as climate change, have a significant impact on the business models and financial activities of companies and financial institutions. Since information on climate change alone is insufficient for both companies and investors in decision-making, the goal was to establish a mechanism for disclosing information on nature and ecosystems as a whole. Thus, the Taskforce on Nature-related Financial Disclosures (TNFD) was established in 2021.

Explanation] What is TNFD? A new bridge between finance and the natural environment

Furthermore, the establishment of TISFD through the merger of TIFD and TSFD is another important topic that highlights the importance of ESG in terms of comprehensive disclosure of inequality and social aspects.

[Commentary] Future Activities of the Task Force on Inequality and Socially Related Financial Disclosures (TISFD)

The SBTN, described in the previous section, is another example of the GHG to ESG shift, as it is an institution established to complement the SBTi framework.

4. conclusion

This paper introduced organizations and indicators involved in GHG emission reductions and the importance of shifting to ESG.

The requirements for corporate activities to realize a sustainable society are changing by the minute. The demand for ESG analysis is expected to continue to grow as companies not only join SBTi, but also become more active in calling on the Japanese government to set more ambitious targets. ESG analysis services provided by aiESG enable sophisticated and diverse ESG analysis through the use of our proprietary AI technology.

aiESG provides support from basic ESG-related standards and frameworks to actual disclosure of non-financial information, so please contact us if you have any ESG-related issues.

Contact us:

https://aiesg.co.jp/contact/

References

[1]https://wmo.int/news/media-centre/global-temperature-likely-exceed-15degc-above-pre-industrial-level-temporarily-next-5-years

[2]https://www.un.org/en/climatechange/events/world-environment-day-2024/live-blog

[3]https://sciencebasedtargets.org/news/the-sbti-releases-new-reports-to-help-accelerate-corporate-climate-action-beyond-the-value-chain

[4]https://ghgprotocol.org/blog/land-sector-and-removals-workstream-update

[5]https://www.cdp.net/en/articles/investor/367-financial-institutions-and-multinational-companies-worth-33-trillion-join-forces-to-demand-science-based-targets-in-race-to-15c

[Related Article.

Report List : Regulations/Standards

Explanation] What is TNFD? A new bridge between finance and the natural environment

[Commentary] TISFD: Task Force on Inequality and Social-related Financial Disclosures

[Commentary] SBTs for Nature -Science-Based and Nature-Related Goals