INDEX

Since the release of the final recommendations of the Task Force on Nature-related Financial Disclosures (TNFD) on September 18, 2023, this website has provided the background and overview of the recommendations and the issues involved in actual disclosure in the past three issues.

Part 1 What is TNFD? A new bridge between finance and the natural environment

2nd TNFD disclosure status and issues

Part 3: Key Points of the TNFD Final Recommendations and the Responses Required of Companies

In this issue, we will focus on the disclosures that companies are actually making about TNFD early adopters and their characteristics, as announced at the Davos meeting on January 16, 2024.

TNFD Early Adopters and Disclosure Reports

The TNFD published its final recommendations in September 2023, and companies that will begin disclosures based on these recommendations by FY2025 are announced as early adopters.

320 companies from 46 countries were announced as early adopters, of which 80, or a quarter of the total, were Japanese companies.

Below are 26 Japanese companies that have registered as TNFD early adopters as of February 2024 and have already published TNFD reports. (Table 1)

| sector | business | Report |

| Food & Beverage | monosodium glutamate (brand name) | biodiversity |

| Asahi Group Holdings, Ltd. | Sustainability Report | |

| Kirin Holdings Company, Limited | Environmental Report 2023 | |

| Suntory Foods International Ltd. | Disclosure based on TNFD recommendations | |

| Nissui | TNFD Report 2023 | |

| Meiji Holdings Co. | biodiversity | |

| nissin foods holdings inc. | biodiversity | |

financing | Asset Management One | Sustainability Report |

| Dai-ichi Life Holdings, Inc. | Integrated Report 2023 | |

| The Norinchukin Bank | Sustainability Report 2023f | |

| Sumitomo Mitsui Financial Group | 2023 TNFD Report | |

| MS&AD Insurance Group Holdings, Inc. | TCFD and TNFD Report | |

| Resona Asset Management | Climate/Nature-related Financial Disclosure Report | |

| communication | NTT Data Group | Environmental Report |

| KDDI | TNFD Report 2023v1 | |

| SoftBank (Japanese telecommunications company) | Biodiversity Conservation | |

| real estate | tokyu land holdings inc. | TNFD Report |

| Sekisui House | Value Report 2023 | |

| rubber | Bridgestone | TCFD/TNFD Comparison Table |

| Sumitomo Rubber Industries, Ltd. | Response to TNFD | |

| air transportation | Japan Air Lines | P Integrated Report |

| infrastructure | Kyushu Electric Power Co. | TNFD Report 2023 |

| electronic goods | NEC | TNFD Report 2023 |

| chemistry | Sekisui Chemical | TCFD and TNFD Report |

| trading company | Sumitomo Corporation | ESG Communication Book 2023 |

| construction | Sumitomo Forestry | Biodiversity Conservation |

Disclosure Features

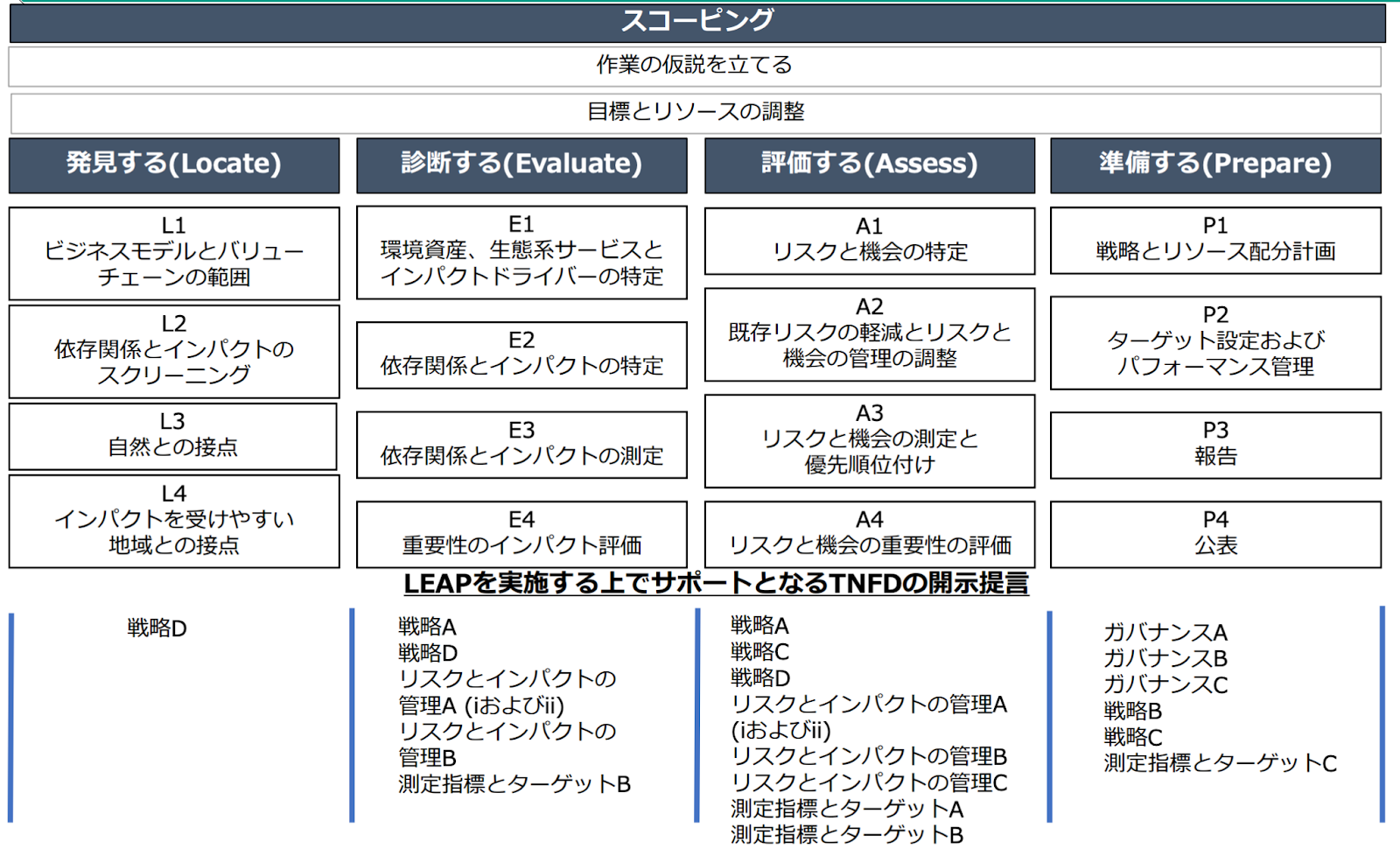

In actual TNFD disclosures, many companies are following the disclosure recommendations and classifying their disclosures into governance, strategy, risk and impact management, and metrics and targets. Companies that are conducting trial analysis or disclosing TNFD reports as beta versions are beginning to follow the framework of the LEAP approach.

The Ministry of the Environment has organized each phase of the LEAP approach by linking it to which disclosure recommendations it corresponds to (Figure 1). (Figure 1)

Figure 1: Source: Ministry of the Environment, "LEAP/TNFD Explanation Workshop for Nature-related Financial Information Disclosure 《Advanced Edition》"

The following is a summary of the tools and analytical procedures used for each of the four pillars of disclosure recommendations in an actual company's TNFD report disclosure. The governance section is omitted as it follows the TCFD.

1. strategy

a. Understanding dependence on and impact on natural capital

To understand the dependence on and impact of natural capital, a heat map was created using tools and indicators such as ENCORE and NBI, and a 4-point scale was used to identify projects that are dependent on nature and have a high impact on nature-related risks.

b. Risk assessment for natural capital

Items that score high from the results of the dependency and impact assessment and items that are risky from a business perspective are identified and organized into physical risks and transition risks. In assessing risk, the following tools are often used for each nature-related risk.

(1) Water: AQUEDUCT, Water Risk Filter

(2) Biodiversity: IBAT, J-BMP, BiomeViewer, KBA

(3) Forest: WBCSD, Biodiversity Risk Filter

c. Opportunities

Describe biodiversity initiatives in which the business can play to its strengths, support for nature-positive initiatives, etc.

2. risk and impact management

Include a description of efforts to mitigate identified risks, establishment of risk management rules and regulations, and internal governance structure.

3. metrics and targets

Many companies have already disclosed figures in their TCFD and environmental reports, etc. Few companies have yet to make disclosures based on the Global Core Disclosure Indicators that are strongly required to be disclosed in the TNFD.

TNFD disclosure issues

However, there are a wide range of reports, including those for each disclosure proposal, for each element of LEAP, and for reports that do not clearly distinguish the categories, and there are hurdles in making side-by-side comparisons from company to company.

With regard to the last of the four pillars, the disclosure of metrics and targets, while some companies are disclosing ESG-related data as required by the TCFD and other regulations, very few are disclosing data in the form of core indicators as required by the TNFD, and it is clear that data aggregation itself is an issue. It is clear that the aggregation of data itself poses a challenge.

The issues raised by the companies that have actually implemented TNFD disclosure include the difficulty of setting up and disclosing scenarios for each business on their own in the absence of normative disclosure, the need for guidance on LEAP analysis because of the challenge of identifying priority areas for conglomerates with a wide range of business domains, and the lack of clarity in the definition of what is meant by core indicators when disclosing core indicators. In addition, the definitions of what the indicators mean are unclear when disclosing core indicators.

Although the framework in TNFD disclosures has been established, detailed item-by-item interpretations and definitions remain unclear, and a better understanding of definitions is needed to ensure comparability among companies.

Examples of corporate TNFD disclosures

As an actual disclosure case study, we will focus on Nissui. Nissui isGroup Integrated ReportIn the "Businesses that are dependent on natural capital, we believe it is necessary to look at the relationship with natural capital from a larger perspective than just the fisheries resource surveys we have been conducting," it is stated in the "Businesses that are dependent on natural capital, we believe it is necessary to look at the relationship with natural capital from a larger perspective than just the fisheries resource surveys we have been conducting. Using the LEAP approach proposed in the TNFD (Nature-related Financial Disclosure Task Force) disclosure framework on a trial basis, the report deciphers the relationship between dependence on and impacts from nature, analyzes risks and opportunities, and examines measures to address them.

Nissui

| process | summary |

| Scope | Identified the scope for adopting LEAP using the Science Based Targets Network (SBTN). Evaluated the natural impacts of the value chain and the company's operations and set the scope of analysis. |

| Locate | Identify the marine areas from which your company procures marine products as priority areas using FAO. |

| Evaluate | Using ENCORE, the primary assessment of the relationship between dependence on and impact of nature on fisheries and aquaculture operations was conducted. A secondary assessment (qualitative assessment) was conducted again, taking into account the actual situation of the company's own operations and upstream value chain. |

| Assess | Physical risks, transition risks, and opportunities in fisheries and aquaculture, respectively. The impact arising from these risks and opportunities is also described. |

| Prepare | Describe measures to mitigate risks, development systems to realize business opportunities, etc. |

Detailed scenarios and rationale are provided in the Scope process, which explains why fisheries and aquaculture projects were included in the evaluation.

Due to the limitation that ENCORE is not able to conduct an analysis that reflects the characteristics of the company's business, a qualitative evaluation was also conducted as a secondary evaluation, and the impact and dependence of the company's business on natural capital was described in an easy-to-understand manner.

The company also discloses Core Global Core Indicators, which is a step forward in TNFD disclosure.

Direction of corporate response

At the 15th Conference of the Parties (COP15) to the Convention on Biological Diversity held in December 2022, international biodiversity targets for 2030 and 2050 were adopted. In light of the number of TNFD early adopters announced at the Davos meeting, the number of companies disclosing TNFD is sure to increase in the future. It is also important to note that, as with the TCFD recommendations, it is possible that in the future, companies may be required to base their sustainability information disclosures on the TNFD recommendations.

The services provided by aiESG enable ESG analysis not only on a company or business unit basis, but also on a product or service basis. In addition to indicators such as greenhouse gas emissions, which can be measured by conventional services, aiESG can also quantitatively capture social and natural environmental aspects required by the TNFD, including community impacts and indigenous peoples' rights. In addition to GHG emissions and other indicators that can be measured by conventional services, the TNFD also quantitatively captures social and natural environmental aspects required by the TNFD, such as community impacts and indigenous rights. Furthermore, for each of these items, it is possible to identify hotspots in the supply chain where risk is high, leading to the identification of priority areas of high risk.

Because it is difficult to reach disclosure overnight in this framework, it is necessary to first reaffirm the challenges of one's own business and discuss disclosure from the point at hand, so as not to fall behind the industry and social trends.

aiESG provides support from the basics of TNFD to the actual disclosure of non-financial information, so if your company is having trouble with TNFD, please contact us.

Contact us:

https://aiesg.co.jp/contact/

Related page

Report List : Regulations/Standards

https://aiesg.co.jp/topics/report/tag/基準-規制/

【【Explanation] What is TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/topics/report/230913_tnfdreport/

Commentary] TNFD Disclosure Status and Issues

https://aiesg.co.jp/topics/report/230102_tnfdreport2/

Commentary] Key Points of the TNFD Final Recommendations and the Responses Required of Companies

https://aiesg.co.jp/topics/report/231106_tnfdreport3/

Nature Positive: Realizing a Society that Can Live in Harmony with Nature

~About OECM and natural symbiosis sites~.

https://aiesg.co.jp/topics/report/240214_nature-positive/

The TNFD commentary book "TNFD Corporate Strategy - Nature Positive and Risk/Opportunity", written in part by aiESG, will be published.

https://aiesg.co.jp/topics/news/2400228_tnfd-publication/