INDEX

On April 23, 2024, the International Sustainability Standards Board (ISSB) announced that biodiversity, ecosystems and ecosystem services (BEES), and human capital will be key themes for the next two years. Human rights were postponed. Human rights have been postponed.

This paper discusses the background of this announcement, the reasons for the selection of these two themes, and their future impact on Japan.

Background of the Study

On May 4, 2023, the ISSB published a call for input on its agenda priorities for the next two years.

Under one of the three themes addressed in the Agenda Consultation, "Prioritization, Scope and Composition of Potential New Research and Standard Setting Projects," three themes (1) Biodiversity, Ecosystems and Ecosystem Services (BEES), (2) Human Capital, and (3) Human Rights, and "Integration in Reporting" Projects were presented and comments were solicited over a period of approximately four months.

The result,(1) Biodiversityand(2) Human capitalThe theme was adopted based on the market's growing need for the disclosure of the company's financial information as a major source of value for the company.

IFRS S1 already requires disclosure of material information about risks and opportunities in sustainability, and guidance, including SASB standards, should be consulted when making appropriate disclosures other than climate change.

With this project, we have set out to evaluate and define the limitations of financial disclosures on sustainability and to begin our own standard-setting work in a manner that complements existing guidance.

The next section discusses the background to the adoption of biodiversity and human capital.

2 . Background of the adoption of biodiversity and human capital

◆Biodiversity, ecosystems and ecosystem services

(BEES: Biodiversity, ecosystems and ecosystem services)

IFRS Public DocumentsThe definition of BEES, according to the

biodiversity: refers to the displacement between all living organisms and is a fundamental feature of natural systems.

ecosystemA dynamic complex in which the plant, animal, and microbial communities and their surrounding nonliving environment interact to form a single functional unit, as in temperate deciduous forests, tropical rainforests, forest peat, etc.

Ecosystem ServicesEcosystems: the contribution of ecosystems to the benefits used in economic and other human activities. Examples include climate regulation, raw material and water supply, pollination, and flood prevention.

The document shows that changes in BEES can have a significant impact on corporate risks and opportunities; while BEES supports all human activities, its effective maintenance, preservation, and recovery are compatible relationships that depend on humans.

While enormous economic value is created by nature and the ecosystem services it produces, most ecosystems around the world are in retreat, pointing to the urgency of financial risk.

This was identified as a priority topic due to the significant pace at which related research and work is progressing in this context and the growing need for information from investors.

A set of established and internationally recognized disclosure practices, tools, and metrics have not yet been developed to understand how BEES affects a company's financial position, performance, and prospects in the short, medium, and long term.

In addition, topics and subtopics are not defined or categorized, and a lack of consensus toward setting standards is also noted.

It was also noted that the risks and opportunities associated with BEES vary widely across various geographic locations, business models, economic activities, etc., and the challenges faced vary among companies.

Hence, there is a new need for a flexible framework setup that does not fit into existing frameworks.

◆Human Capital

ISSB Public DocumentsAccording to,human capitalrefers to the people who make up a company's workforce, as well as individual workers' competencies, capabilities and experience, and willingness to innovate.

Investors are increasingly demanding disclosure of human capital because investment in and management of a company's workforce has a direct impact on a company's ability to deliver value over the long term.

Investors are particularly concerned about diversity, equity, and inclusion (DEI), and the Value Reporting Foundation, a division of the IFRSHome PageWe point out in

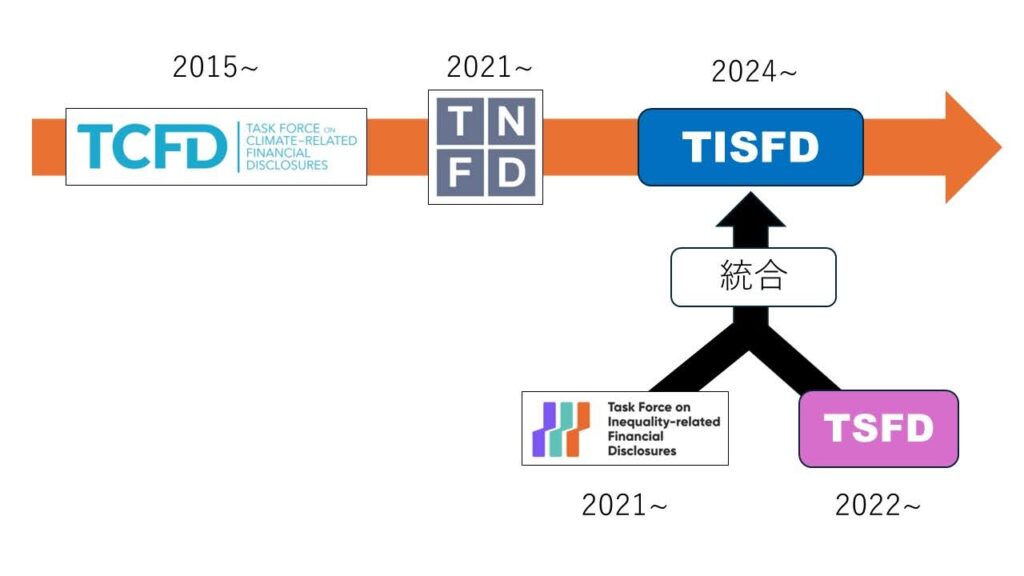

The TCFD and TNFD laid the groundwork for discussions on the environmental aspects of ESG, and later the TIFD and TSFD, which support disclosure of social aspects such as human capital and human rights, were integrated to form the TISFD*. Against the backdrop of this trend, reporting on corporate human capital is also on the rise, as the importance of not only the environment but also the social aspects of companies is increasingly emphasized in ESG.

Figure 1: TISFD inauguration process (prepared by the author)

At the same time, however, investors have voiced a lack of sufficient information to help them make investment decisions. One issue, for example, is the lack of clarity about the difference between human capital and human rights, two topics that have been discussed in the past.

Over the next two years, ISSB's project aims to establish clearer criteria for determining the boundaries and relevance of both topics, as well as conduct research to develop a new human capital framework and improve understanding of related information.

Both BEES and human capital have diverse issues and associated subtopics, which have relevance to various standards, including the TNFD, as described below.

Table 1: Standards used/recommended for reference by ISSB in biodiversity and human capital considerations

interpoint (interword separation)the Capitals CoalitionCapital: Organizations that promote a capital approach

interpoint (interword separation)CDSB Framework: Standards for disclosing environmental and climate information to investors in the company's mainstream reports.

interpoint (interword separation)the EU Business and Biodiversity PlatformBiodiversity in the EU: an organization that provides a forum for discussing the link between business and biodiversity in the EU.

interpoint (interword separation)the European Commission's Align Project (Aligning accounting approaches for nature)Project to: provide principles and criteria for the measurement and assessment of biodiversity to businesses and financial institutions

interpoint (interword separation)EFRAGThe European Commission is the body that reports to the European Commission on financial and sustainability issues.

interpoint (interword separation)GRI StandardsCriteria for the disclosure of information on the organization's economic, environmental, and social impact to multiple stakeholders.

interpoint (interword separation)ILOThe United Nations is an organization that promotes the right to work, encourages decent employment opportunities, enhances social protection, and strengthens dialogue on work-related issues.

interpoint (interword separation)Integrated Reporting FrameworkThe organization aims to promote integrated corporate reporting.

interpoint (interword separation)PBAF: Organizations that provide guidance for financial organizations on assessing biodiversity impacts and dependencies.

interpoint (interword separation)SASB Standard: Criteria for companies to disclose information on sustainability risks and opportunities to investors.

interpoint (interword separation)the Science Based Targets Network: An organization whose goal is to create a global economy in which businesses and governments function in accordance with the greenhouse gas emission reduction targets required by the Paris Agreement.

interpoint (interword separation)TNFDThe standard for disclosing nature-related information that has a financial impact in annual financial reporting.

interpoint (interword separation)the United Nations Declaration on the Rights of Indigenous Peoples: An organization that seeks to ensure the survival, dignity and wellbeing of indigenous peoples.

interpoint (interword separation)the US Securities and Exchange CommissionThe organization supports investors' decision-making through information sharing between companies and investment professionals to ensure fairness in the securities markets and with investors.

interpoint (interword separation)WEF: An organization dedicated to improving world affairs through cooperation between both the public and private sectors.

interpoint (interword separation)the World Benchmarking AllianceOrganizations seeking to change the way business impact is measured in order to motivate companies

Explanatory reports on some of these criteria are available on this website.

interpoint (interword separation)Commentary] Current Status of SASB Standards and Adopted Japanese Companies

interpoint (interword separation)Commentary] Alphabet Soup - Disruptions and Convergence of Sustainability Standards

interpoint (interword separation)What is the SASB Standard for ESG Information Disclosure? (Part 1)Outline of SASB

interpoint (interword separation)What is the SASB Standard for ESG Disclosure? (Part 2) Benefits for Companies

interpoint (interword separation)Explanation] What is TNFD? A new bridge between finance and the natural environment

*TISFD Commentary Article:[Commentary] TISFD: Task Force on Inequality and Social-related Financial Disclosures

◆Human Rights

As a result of the call for comments, the discussion on human rights* was not adopted at this time.

However, the launch of the TISFD has also had an impact, and investors are increasingly demanding disclosure of human rights-related information, as well as human capital.

ISSB research shows that investors are highly concerned about workers' and community rights in a company's value chain.

The former includes health and safety, forced labor, etc., while the latter includes indigenous rights and impacts on land and water.

Human rights values vary widely from country to country and region to region, and the debate that develops in the value chain also varies by business model and sector.

Therefore, it will be necessary to further clarify the boundaries and linkages between human capital and human rights projects and mature our understanding of human rights risks and opportunities in the marketplace by practicing a variety of research, including the development of new human rights-related frameworks.

3. Impact on Japan

The application of the SSBJ standards, which are consistent with the ISSB standards, to securities reports is scheduled to become mandatory for companies with a market capitalization of 3 trillion yen or more as early as March 2027.

The SSBJ standards are supposed to be consistent with the ISSB standards, and it is highly likely that the SSBJ will develop new standards in line with the ISSB's agenda and reflect them in the disclosure in its securities reports.

In a report* recently released by aiESG, it is noted that since the mandatory disclosure of human capital information in Japanese securities reports began in 2023, there has been an increase in demand for corporate disclosure of not only environmental aspects but also social aspects.

The ISSB's work schedule for the next two years is scheduled to be released in June of this year, which may further accelerate the movement toward information disclosure in the Japanese domestic market.

*aiESG Report:Commentary] The Importance of Social and Human Capital in Securities Reports

4. Conclusion

This paper examines the background and future prospects for the ISSB's consideration of biodiversity and human capital over the next two years.

The ISSB also emphasizes the relevance of relevant existing frameworks (e.g., SASB Standards, CDSB Guidance, GRI Standards, etc.) and considers their relevance to the TNFD.

The ISSB's new standard setting through this project will help investors and companies better understand biodiversity and human capital, and enable them to set clearer targets and disclosure work.

aiESG emphasizes not only BEES, but also human capital and human rights disclosure with an eye to the future, and the unique tools we provide will enable us to provide higher quality disclosure.

aiESG provides support from basic ESG-related standards and frameworks to actual disclosure of non-financial information, so please contact us if you have any ESG-related issues.

Contact us:

https://aiesg.co.jp/contact/

References

[1]https://www.ifrs.org/news-and-events/news/2024/04/issb-commence-research-projects-risks-opportunities-nature-human-capital/

[2]https://tnfd.global/tnfd-welcomes-the-issbs-decision-to-commence-work-on-nature-related-issues/

[3]https://www.ifrs.org/content/dam/ifrs/project/issb-consultation-on-agenda-priorities/issb-rfi-2023-1.pdf

[4]https://sasb.ifrs.org/standards/process/projects/human-capital-diversity-equity-inclusion/

[5]https://sasb.ifrs.org/standards/process/projects/human-capital-diversity-equity-inclusion/

Related page

Report List : Regulations/Standards

Commentary] ISSB - Global Baseline for Sustainability Disclosure

Commentary] SSBJ (Sustainability Standards Board Japan) Deliberation Trends - Scope 3 Disclosure Standards in Japan

Commentary] Non-Financial Capital: Trends in Human and Natural Capital - Disclosure Regulations and Guidelines in Japan and Overseas

The Importance of Social Aspects in Nonfinancial Information Disclosure