In recent years, investors in international capital markets have been seeking information that enables them to assess the value of companies.

The ISSB was created to meet this demand.

In this article, we would like to tell you exactly what ISSB is.

What is ISSB?

The International Sustainability Standards Board (ISSB) is the body responsible for setting standards and frameworks for sustainability disclosure.

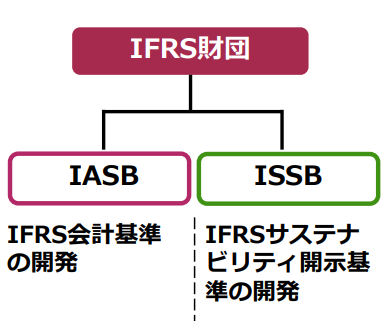

The ISSB was established as a sub-organisation of the IFRS Foundation.

The IFRS Foundation is a not-for-profit organisation dedicated to developing international accounting standards.

The International Accounting Standards Board (IASB), a body under the IFRS Foundation, originally developed the International Financial Reporting Standards (IFRS).

The ISSB was established in parallel with the IASB.

The ISSB has published the IFRS Sustainability Disclosure Standard, which is designed to meet the information needs of investors when assessing corporate value.

Although each organisation operates independently, the combination of financial information by the IASB and non-financial information by the ISSB enables the provision of information that better meets the needs of investors and others.

Figure 1: Organisational chart of the IFRS Foundation

(Source: SSBJ, National and International Initiatives on Sustainability Disclosure Standards).

Background to the establishment of the ISSB

There have been several organisations that have set standards for sustainability disclosures.

Key setting actors include the following organisations

IIRC (International Integrated Reporting Council).

SASB (Sustainability Accounting Standards Board).

GRI (Global Reporting Initiative).

Climate Disclosure Standards Board (CDSB).

∙ TCFD (Task Force on Climate-related Financial Disclosures).

*In June 2021, IIRC and SASB merged to form the Value Reporting Foundation (VRF).

However, as each setting entity developed standards based on the needs of its own key users, consistency and comparability of disclosures could not be ensured.

Figure 2: International sustainability disclosure standards

(Source: Ministry of Economy, Trade and Industry, Towards a Virtuous Circle of Sustainability-related Information Disclosure and Corporate Value Creation)

Such a situation could lead to disruptions in international capital markets.

To address this challenge, there is a need to standardise ESG (environmental, social and governance) information and harmonise reporting requirements.

The establishment of the ISSB was therefore set up and the CDSB and VRF merged.

Other major sustainability standard-setters have also expressed their willingness to work with the ISSB, resulting in a unified sustainability standard.

Composition of the ISSB

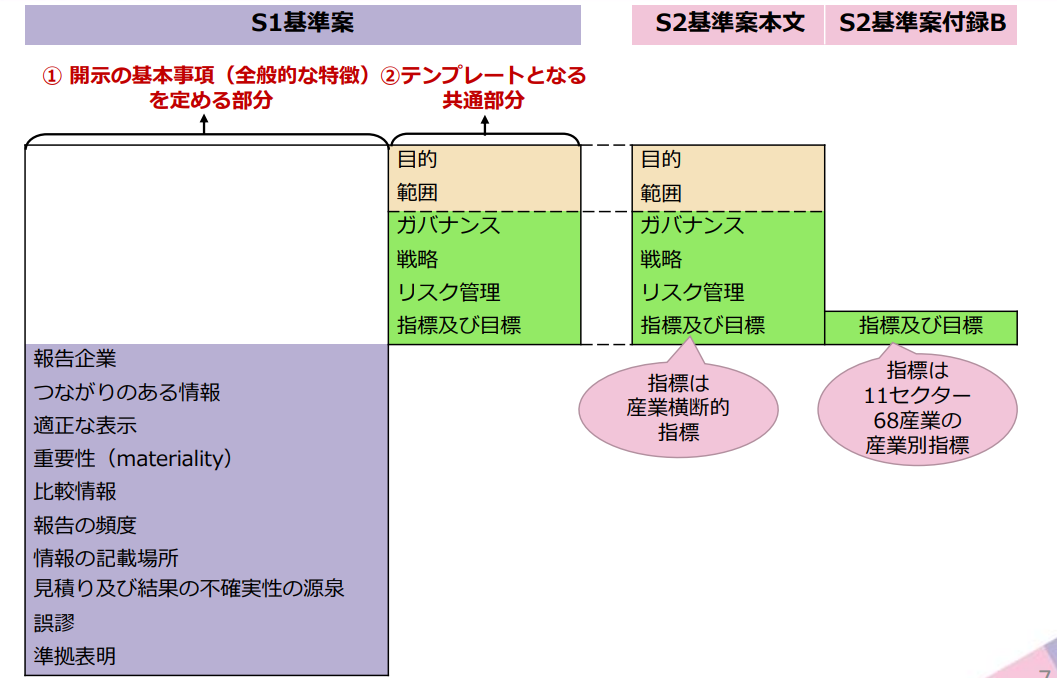

The IFRS Sustainability Disclosure Standard is divided into two sections, IFRS S1 'General Requirements for Sustainability-related Financial Disclosures' and IFRS S2 'Climate-related Disclosures'.

Figure 3: Relationship between IFRS S1 and S2

(Source: SSBJ, National and International Initiatives on Sustainability Disclosure Standards).

IFRS S1, 'General requirements for the disclosure of sustainability-related financial information'.

The objective of IFRS S1 is to require companies to disclose information that is material regarding all significant sustainability-related risks and opportunities.

IFRS S1 is a common presentation standard for IFRS sustainability disclosure standards developed by the ISSB.

It consists of a section setting out the basic matters to be disclosed when preparing sustainability-related disclosures and a section setting out the matters to be disclosed regarding sustainability-related risks and opportunities in the absence of thematic standards (core content).

IFRS S2, 'Climate-related Disclosures'.

The objective of IFRS S2 is to require companies to disclose information that has materiality regarding significant climate-related risks and opportunities that is useful in assessing the value of the enterprise.

IFRS S2 is a disclosure requirement set out in terms of the four elements of the TCFD recommendations: governance, strategy, risk management and indicators and targets.

Industry-specific requirements have also been published, where disclosure requirements are set by industry (11 sectors and 68 industries) based on the SASB (Sustainability Accounting Standards Board).

| sector | Industry Examples. |

| consumer goods | Clothing, ornaments and footwear, household appliances |

| Mining and mineral processing | Coal business, construction materials |

| financing | Asset management and administration services, commercial banking |

| Food and beverages | Agricultural products, alcoholic beverages |

| medical care | Pharmaceutical retailing and healthcare provision |

| infrastructure | Electricity utilities and power producers, house-building industry |

| Renewable resources and alternative energy sources | Biofuels, forest management. |

| resource processing | Aerospace and defence, chemical products |

| service | Casinos and gaming and leisure facilities |

| Technology and communications | Hardware, semiconductors. |

| transport | Air cargo and logistics, airlines |

Table 1: Composition of 11 sectors and 68 industries

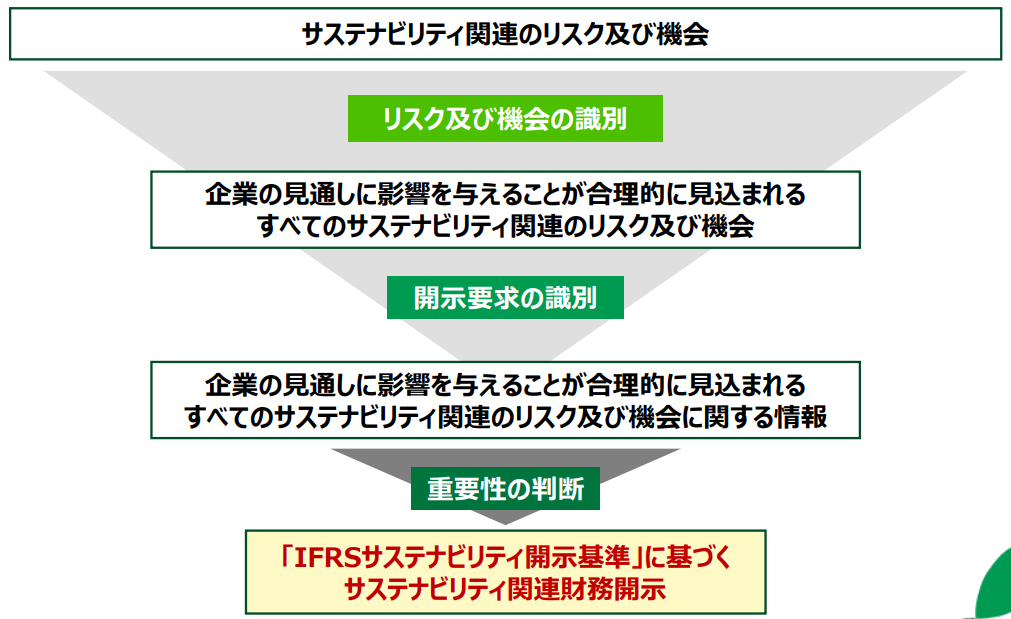

Processes required for ISSB disclosure.

The premise is that the information disclosed by companies should influence investors' decisions.

This section presents the process of creating such disclosures.

The first step is to identify risks and opportunities.

Companies identify various sustainability-related risks and opportunities that are reasonably expected to affect the company's prospects.

The next step is to identify the information disclosed.

Specific disclosures are prepared from the identified risks and opportunities.

In these two steps, the IFRS Sustainability Disclosure Standard is applied.

Finally, a materiality determination is made.

Disclosure information prepared is omitted that is not considered to influence investors' decision-making.

The above process produces disclosures that are useful to investors.

Figure 4: Process for identifying information of importance

(Source: SSBJ, 'Overview of IFRS S1 and IFRS S2')

Conclusion.

The IFRS Sustainability Disclosure Standard issued by the ISSB enables investors to obtain information on risks and opportunities related to corporate sustainability.

The quality of ESG investment is expected to improve as sufficient information reaches investors.

Going forward, the IFRS Sustainability Disclosure Standard is expected to become a comprehensive global baseline for sustainability disclosures.

aiESG can provide support on everything from the basics of ISSB to the actual disclosure of non-financial information. aiESG is happy to assist companies that need help in complying with ISSB.

Enquiry:

https://aiesg.co.jp/contact/

References.

IFRS:IFRS Sustainability Standards Navigator

Sustainability Standards Committee:Overview of ISSB standards, exposure drafts, etc.

Ministry of Economy, Trade and Industry:Interim report of the Study Group on Guidelines for Disclosure of Non-financial Information.

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

Commentary] What is the SASB Standard for ESG Information Disclosure? (Part 1) SASB Overview

https://aiesg.co.jp/report/2301025_sasb1/

[Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/