Previous articleAs we saw in Section 3.1, the importance of social factors in the three ESG factors and the need for human rights DD is being reaffirmed worldwide. In this issue, we look at the developments surrounding the disclosure of information on the social dimension, with a focus on the introduction of the TISFD, which is gaining attention as a new task force following the TCFD and TNFD.

Table of Contents

Hurdles to disclosure of socially relevant information

TISFD: Task Force on Inequality and Social-related Financial Disclosures

TISFD objectives and approach

TISFD and the future of social aspects of information disclosure

Conclusion.

Hurdles to disclosure of socially relevant information

Measuring risks in the social and human rights aspects is not an easy task for many companies, as in the environmental field, where quantitative information disclosure is difficult to visualise. In particular, the current situation where there are numerous international standards to comply with is one of the factors making it difficult for companies to disclose information (Fig. 1).

Figure 1: International standards to which companies developing human rights policies adhere

(Source:Results of the Questionnaire Survey on the Status of Human Rights Initiatives in the Supply Chains of Japanese Companies.)

Many companies also face challenges in the process of 'identifying and assessing negative impacts', which was mentioned in the previous article, and the method of risk analysis that goes back through the supply chain is not widespread [1].

TISFD: Task Force on Inequality and Social-related Financial Disclosures

Amidst a flurry of various human rights-related guidelines and frameworks, the Task Force on Inequality and Social-related Financial Disclosures (TISFD) [2 ], which in April 2023 will be joined by the Task Force on Inequality-related Financial Disclosures (TIFD) and the Taskforce on Social-related Financial Disclosures (TSFD) [2]. Financial Disclosures (TSFD), which, as the name suggests, aims to provide a framework for inequality and social-related risk disclosure.

Following the TCFD on climate change, to which many companies already comply, and the nature-related TNFD, which has attracted interest following the publication of the final recommendations in September, it is expected to provide a clear standard for disclosure of information on the social aspects.

Table 1: Overview of TISFD (prepared by the authors)

| TIFD | TSFD | TISFD | ||

| name | Inequality-related Financial Disclosure Task Force | Task Force on Disclosure of Socially Relevant Financial Information | Integration ⇒ | Inequality and Social Related Financial Disclosure Task Force |

| Year and activities | 2021 Establishment. | 2021 Discussions begin. | Apr 2023. TIFD and TSFD announce merger [3]. Aug 2023. Document publication [4]. First half of 2024 Task Force to be established | |

| Main organisations involved. | Argentine Network for International Cooperation (RACI), Pre-Distribution Initiative (PDI), Rights CoLab, Southern Centre for the Study of Inequalities (SCIS), United Nations Development Programme (UNDP) | Business Coalition for Inclusive Growth (B4IG), OECD | World Business Council for Sustainable Development (WBCSD), Council for Inclusive Capitalism (CIC), Shift [5]. |

TISFD objectives and approach

The TISFD published a text outlining its objectives and approach in August 2023 [6]. It stated there that the following methods would be used to achieve its objectives

1. develop clear disclosure standards, building on existing frameworks

Understand the mutual impacts, dependencies and risks between companies/investors and people.

Promote a common understanding of inequality and social-related issues and design situation-based indicators.

Support interoperability with TCFD and TNFD and align with existing sustainability disclosure standards.

∙ Use frameworks developed by the United Nations, the OECD and others to promote alignment with them.

2. co-operation with international standard-setting bodies

∙ Establish a framework available as a knowledge partner with standard-setting bodies such as the International Sustainability Standards Board (ISSB), the European Financial Reporting Advisory Group (EFRAG) and the Global Reporting Initiative (GRI).

3. contribution to global policy objectives

∙ Cooperate with global policy fora such as the G20 and G7 to contribute to global policy goals, such as the achievement of the Sustainable Development Goals (SDGs).

4. regular review and updating of the framework

Furthermore, in addressing these, the TISFD states that it operates through dialogue with a wide range of stakeholders, including funders and businesses, governments and regulators, international organisations, trade unions, civil society and people affected by inequalities and social harm or benefit.

TISFD and the future of social aspects of information disclosure

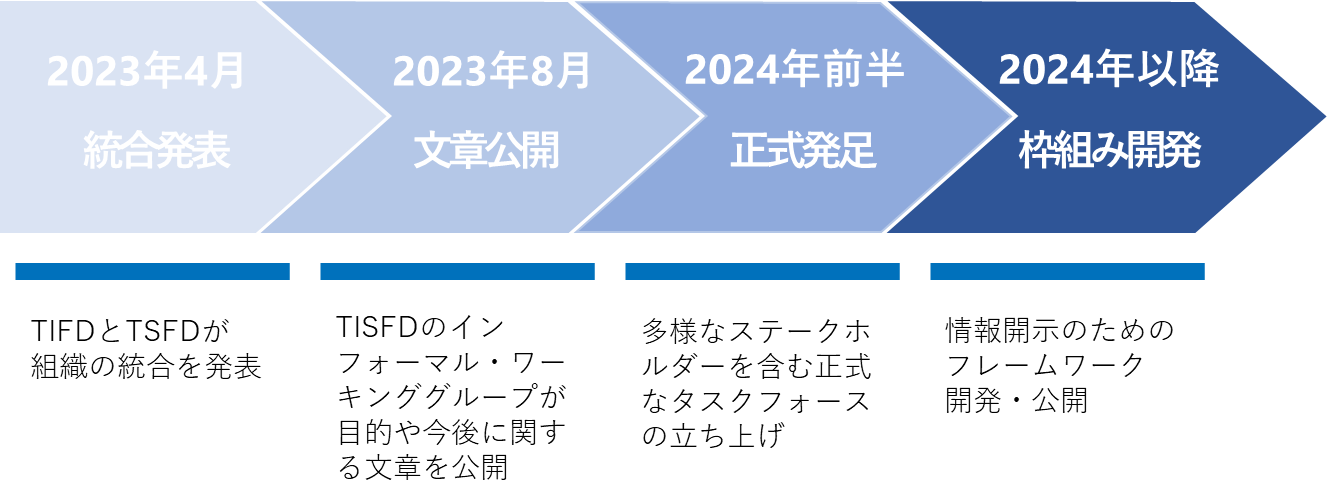

The TISFD is still in its developmental stage and does not already have specifics on information disclosure. According to the above text, the first step is to establish a working group that includes the original members of the TIFD and TSFD, plus a wider range of stakeholders. The working group will set up a task force in the first half of 2024, after which the disclosure framework will be developed.

Figure 2: TISFD schedule of activities (prepared by the author)

Its predecessor disclosure frameworks, the TCFD and the TNFD, took around two years from their establishment to the publication of their recommendations, and it is likely that the TISFD will adopt the same general structure (e.g. the four pillars of disclosure recommendations), so discussions may develop more quickly than before. In addition, the release of beta versions, such as the TNFD, and cooperation with existing initiatives, such as the UN Guidance, may further raise the profile of the final recommendations even before they are released.

While numerous standards exist, it remains to be seen to what extent the TISFD, which is still under development, will become a standard in the international community. However, if the framework is supported by various influential international organisations and has much in common with the TCFD, which is already considered important by many companies, it is expected to become one of the major options for companies considering social aspects of information disclosure.

Conclusion.

This article has provided a detailed introduction to the TISFD, which is attracting attention as a new framework for socially relevant information disclosure.

Following the formulation of the TCFD in 2015, corporate interest in environmental risks has expanded significantly, leading to it becoming practically obligatory. Currently, the disclosure of social aspects of risk is left to the discretion of each company, but a similar trend may occur with the release of the TISFD. In addition, companies will also benefit from prompt compliance with international frameworks in order to respond to human rights DD legislation that is already underway abroad.

Although the TISFD still lacks a full picture, it is important that each company first understands the interface between its business and human rights risks, while referring to the UN Guiding Principles, which are clearly stated to be harmonised.

aiESG can provide support on the TISFD and related frameworks, from the basics to the actual disclosure of non-financial information. companies that need help with the social aspects of ESG disclosure are encouraged to contact us.

Enquiry:

https://aiesg.co.jp/contact/

Bibliography

[1] 20211130001-1.pdf (meti.go.jp).

[2] The names are provisional and subject to change (see below).Taskforce on Inequality and Social-related Financial Disclosures (TISFD) | Groups | LinkedIn)

[3] Joint Statement on Convergence Between TIFD and TSFD - Task Force on Inequality-related Financial Disclosures (TIFD) (thetifd.org)

[4] Taskforce on Inequality and Social-related Financial Disclosures (TISFD) | Groups | LinkedIn

[5] Research institute for the 'UN Guiding Principles on Business and Human Rights'.

[6] https://www.linkedin.com/feed/update/urn:li:activity:7102273687029972992?utm_source=share&utm_medium=member_desktop

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

Commentary] The importance of social aspects in non-financial information disclosure.

https://aiesg.co.jp/report/2301214_tisfd1/

[The [ibid.Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/

Commentary] What is the SASB Standard for ESG Information Disclosure? (Part 1) SASB Overview

https://aiesg.co.jp/report/2301025_sasb1/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/