(Summary)

The European Sustainability Reporting Standards (ESRS) aim to improve the quality and comprehensiveness of corporate sustainability reporting and promote sustainable development through transparency.

The ESRS is an integral part of the delegated rules of the Corporate Sustainability Reporting Directive (CSRD). This means that if you are a company covered by the CSRD, you will have to adopt the reporting standards set out by the ESRS.

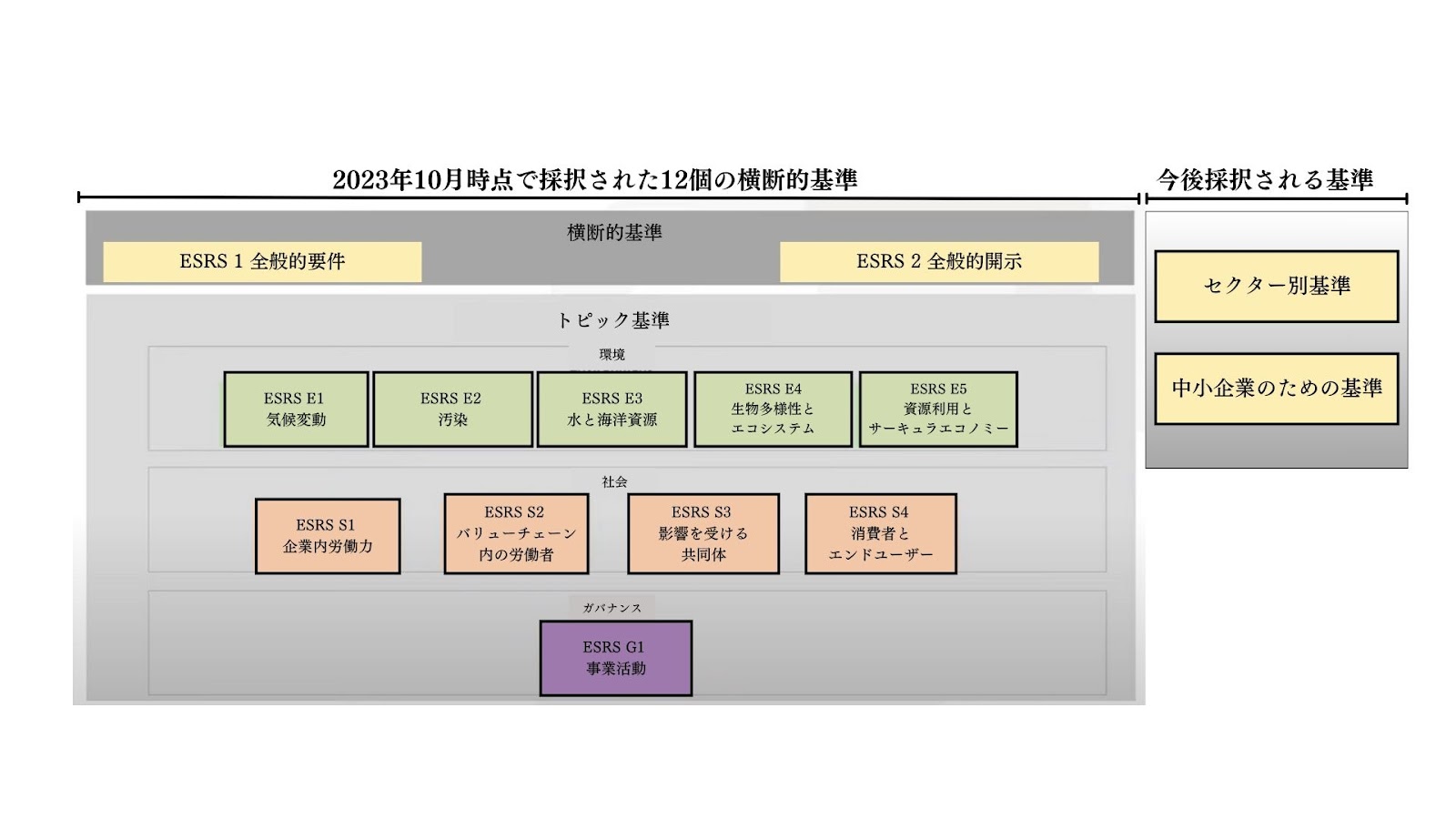

A revised version of the ESRS was published in June 2023 and adopted by the European Parliament and the European Council in October 2023. The ESRS published at present consists of 12 standards which are defined as cross-industry standards. Broadly speaking, there are two 'cross-cutting criteria' and ten 'topic criteria'. This one serves as a common standard that all companies subject to the CSRD must comply with.

Looking ahead, 'sector (industry) specific standards' and 'standards for SMEs' will be established as components of the ESRS.

The purpose of this paper is to provide a brief description of the ESRS cross-cutting standards that are currently known.

Please refer to the previous article on CSRD commentary for a more in-depth understanding of the role of the ESRS and the state of sustainability reporting in the EU.

Commentary] CSRD: the EU version of the sustainability reporting standard just before it enters into force.

~The impact on Japanese companies~.

https://aiesg.co.jp/report/2301120_csrd/

Table of Contents

(Summary)

1. the purpose of the ESRS

2. currently published ESRSs

Image 1: Schematic diagram of the ESRS as currently published.

ESRS1: General requirements

ESRS 2: General disclosures

Table 1: Matters covered by ESRS topics (prepared by the authors from ESRS drafts)

ESRS E1~E5: Environmental aspects

ESRS S1~S4: Social aspects

ESRS G1: Governance aspects

3. summary and future perspectives

Objectives of the ESRS

A major objective of the ESRS is the continuous improvement of corporate sustainability performance and management through enhanced sustainability reporting.

The ESRS places an obligation on companies to report on their supply chain and product lifecycle impacts, as well as the extent of their impact on the consumer side, environmental and social aspects, etc., according to key requirements.

As an objective statement for the disclosure of non-financial information, the EU has introduced the concept of 'double materiality' in both CSRD/ESRS standards. Briefly explained, this means that non-financial information should be disclosed to multiple stakeholders (including society and the environment), with the EU's intention of making it clear how a company's own economic activities impact on the environment (E), society (S) and governance (G).

Due to the nature of the ESRS being applied in conjunction with the CSRD, companies applying the CSRD do not need to prepare a separate report for the ESRS.

Currently published ESRS.

The ESRS has now been published in a revised version (https://www.efrag.org/lab6?AspxAutoDetectCookieSupport=1 ), 12 cross-cutting criteria are defined. The term 'cross-cutting' here means 'imposed on all companies applying the CSRD, regardless of sector' and can be seen as a prerequisite for the ESRS, setting out more specifically the principles of the CSRD and the rules to be followed in reporting.

As Figure 1 shows, the currently adopted cross-cutting standards comprise two standards - ESRS 1: General requirements and ESRS 2: General disclosures - and ten topic standards.

Figure 1: Overview diagram of the ESRS as currently published (adapted from EFRAG agency presentation material and translated into Japanese by the author). https://youtu.be/a1pdAO62bH0?si=8ll6e5PhxkR03mF3 )

*ESRS1: General requirements

It sets out principles for the preparation and disclosure of sustainability reports in the application of the CSRD (not including specific report content). It obliges companies to conduct an assessment based on the principle of double materiality. Requires materiality assessments to be made in individual standards, with the exception of the ESRS2, which will be discussed below.

*ESRS2: General disclosures.

It sets out the general features, including policies and objectives, that should be reported regardless of the outcome of the materiality assessment. It also details the structure and content of the ESRS topic criteria, including 'Governance', 'Strategy', 'Management of Impacts, Risks and Opportunities' and 'Evaluation Criteria and Objectives'. These four pillars are in line with existing international sustainability standards frameworks such as the TCFD and the ISSB Framework.

Table 1 summarises the items specified as annexes to each of the topic criteria. Each is specified in three categories: environmental, social and governance.

Table 1: Matters covered by ESRS topics (prepared by the authors from ESRS drafts)

| [Draft].ESRS Topic. | Sustainability matters covered by ESRS topics. | ||

| subject | supplementary item | supplementary information | |

| ESRS E1. | climate change | Climate change adaptation, climate change mitigation and energy | |

| ESRS E2. | pollution | ∙ Air pollution, water pollution, soil pollution, pollution of biological and food resources, substances of concern and substances of very high concern | |

| ESRS E3. | Water and marine resources | Water withdrawal, water consumption, water use, water discharge in water bodies and oceans, habitat degradation and the intensity of pressure on marine resources. | |

| ESRS E4. | Biodiversity and ecosystems. | Direct factors affecting biodiversity loss. | ∙ Climate change, land use change, direct exploitation, invasive alien species, pollution, other |

| Impact on species status. | E.g.: - Species population numbers - Global extinction risk level of a species. | ||

| Impacts on the extent and condition of ecosystems. | Examples: - Land degradation, desertification, soil cover | ||

| Impacts on and dependence on ecosystem services. | |||

| ESRS E5. | circular economy | Resource inflows, including resource use; resource outflows and waste associated with products and services. | |

| ESRS S1. | company-internal workforce | Working conditions. | -Stable employment, working hours, decent pay, social dialogue, freedom of association, existence of employee representative committees, workers' right to information, consultation and participation, collective bargaining (including the proportion of workers covered by collective agreements), work-life balance, health and safety. |

| Equal treatment and opportunities for all | -Gender equality and equal pay for work of equal value; -Training and skills development; -Employment and inclusion of persons with disabilities; -Violence and harassment measures in the workplace; -Diversity. | ||

| Other job-related rights. | ∙ Child labour, forced labour, improved living conditions, privacy | ||

| ESRS S2. | Workers in the value chain | Working conditions. | -Stable employment, working hours, decent wages, freedom of association including social dialogue and the existence of works councils, collective bargaining, work-life balance, health and safety. |

| Equal treatment and opportunities for all | Gender equality and equal pay for work of equal value; training and skills development; employment and inclusion of persons with disabilities; workplace violence and harassment prevention; diversity. | ||

| Other job-related rights. | Child labour, forced labour, housing, water and sanitation, privacy | ||

| ESRS S3. | Affected communities | Economic, social and cultural rights of local communities. | ∙ Housing and food adequacy, water and sanitation, land-related impacts, security-related impacts |

| Civil and political rights of local communities. | Impact on freedom of expression, freedom of association and human rights protection activists | ||

| Specific rights for indigenous communities. | ∙ Free, prior and informed consent, self-determination and cultural rights | ||

| ESRS S4. | Consumers and end-users | Information-related impacts on consumers and end-users. | Privacy, freedom of expression and access to adequate information |

| Personal safety of consumers and end-users. | ∙ Health and safety, personal safety and child protection. | ||

| ... social inclusion of consumers and end-users. | Elimination of discrimination, ensuring access to goods and services, responsibility for marketing activities | ||

| ESRS G1. | business activities | ∙ Managing supplier relationships, including corporate culture, whistleblower protection, animal welfare, political engagement and lobbying, and payment practices. | |

| Corruption and bribery. | Prevention and detection/accidents, including training |

*ESRS E1~E5: Environmental aspects

The five environmental standards include reporting on climate change, pollution, water and marine resources, biodiversity and ecosystems, and resource use and the circular economy. Companies are also required to disclose their approach to transitioning to sustainable business models and their corresponding plans. In addition, it imposes the need to report on the company's efforts to support the environmental objectives of the EU Green Deal.

*ESRS S1~S4: Social aspects

The four social standards require companies to systematically disclose data on their internal employees as well as external stakeholders. One of the standards focuses in particular on employees within the value chain. In addition, details about communities and consumers/end-users who are considered to be affected by the company's operations are also dealt with in the individual standards. In S2~S4, the focus is on qualitative information only.

*ESRS G1: Governance aspects

The Governance Standards detail the responsibilities of governance through a better understanding of the approach, operations and results of the entity. It also outlines reporting requirements to manage impacts, risks and opportunities. In addition, they require disclosure of the company's fundamental policies and corporate culture, and include anti-corruption measures, supplier relationships, plus political involvement in the disclosure requirements.

Summary and future perspectives

The ESRS aims to improve the quality and comprehensiveness of corporate sustainability reporting and promote sustainable development through transparency; companies applying the CSRD are required to adopt the reporting standards set out by the ESRS.

In the coming months, the Commission and the Council will discuss and prepare sector-specific standards and standards for SMEs. The sectors for the sector-specific standards currently known are as follows.

Oil and gas

Coal, quarries and mining

Road transport

Agriculture, dairy farming and fishing

Motor vehicles

Energy production and utilities.

Food and beverages.

Apparel and jewellery.

To begin with, after discussing the provisions for the oil and gas sector, the overall application of sector-specific standards is scheduled to start in 2026.

As the CSRD will start applying to SMEs from 2026, it is planned that the standards for SMEs will be addressed before then. The standards for SMEs will be addressed by then.

aiESG provides support on CSRD, from the basics to the actual disclosure of non-financial information. aiESG is happy to assist companies that need help with CSRD compliance.

Enquiry:

https://aiesg.co.jp/contact/

*Related page*.

Commentary] CSRD: the EU version of the sustainability reporting standard just before it enters into force.

~The impact on Japanese companies~.

https://aiesg.co.jp/report/2301120_csrd/

Commentary] What is the SASB Standard for ESG Information Disclosure? (Part 1) SASB Overview

https://aiesg.co.jp/report/2301025_sasb1/

[Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/