Concepts such as human capital and natural capital have been rapidly gaining ground in recent years. This is a movement to regard human resources and the environment not as costs or resources as they have been perceived in the past, but as 'capital' that can be used to fund corporate activities, and to disclose this to the market as an object of investment.

This article provides an overview of national and international disclosure regulations and guidelines on these developments surrounding non-financial capital, and introduces the concept of 'impact-weighted accounting', whereby these are converted into monetary terms and reflected in the financial statements.

Importance of non-financial capital.

Unlike in the days when manufacturing was the main source of profit from the production of goods, today, when the focus of industry has shifted to the service industry and social interests and investment values have become more diverse, it has become more difficult to judge company value solely on the basis of existing figures on financial statements. In order to increase the value of a company based on sustainability in changing circumstances, it is necessary to regard excellent human resources and environmental arrangements as 'capital' and to actively make them investment targets.

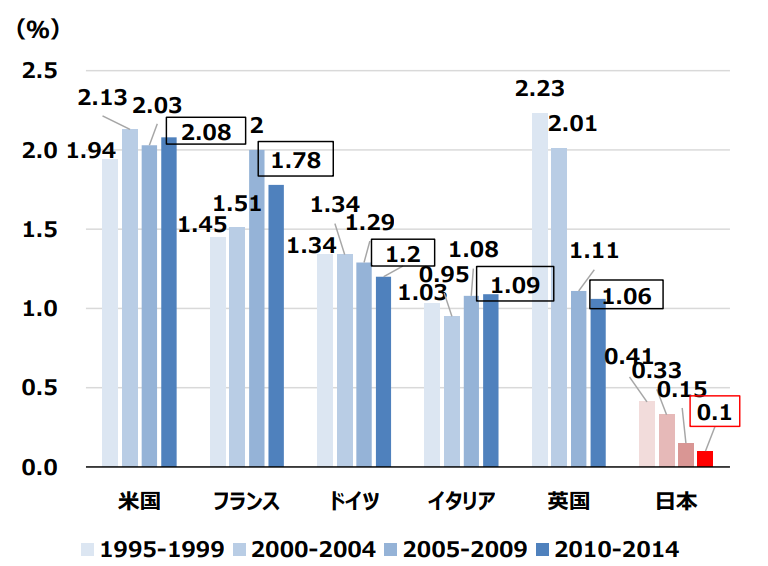

One example of the importance of non-financial capital is human resource development. In Europe and the USA, where human resources are fluid, it is essential for people to learn and grow after they start work, whereas Japanese companies have not invested sufficiently in human resources for a long time. Figure 1 compares the ratio of human investment to GDP in different countries.

Figure 1: International comparison of human resources investment (other than OJT) (% of GDP) (Source:Ministry of Economy, Trade and Industry)

This shows that Japan's human resources investment ratio is notably lower than in the West.

A comparison of PBR (price book value ratio), which is a value indicating the market capitalisation of a company's shares relative to its net assets, by industry in Japan, the US and Europe shows that Japanese companies have the lowest average PBR in all industries (as of March 2022) [1]. Companies with a PBR below 1 are considered to have non-financial capital other than financial net worth that is negatively valued in the market (Fig. 2).

Figure 2: Average PBR by industry sector in Japan, the US and Europe (Source:Ministry of Economy, Trade and Industry)

This data is thought to be due to the relatively low level of interest in human capital and other aspects of Japanese companies, as well as the fact that the initiatives being taken within companies are not being disclosed in an appropriate manner.

Elements of human and natural capital

When it comes to human capital and natural capital, different companies and organisations have different definitions of these terms and there is a wide range in the scope of what is assumed. Here we quote from the International Integrated Reporting Framework published by the International Integrated Reporting Council (IIRC) [2], which explains.

◾️ Human capital: people's ability, experience and willingness to innovate, e.g,

Attunement to and support for organisational governance frameworks, risk management approaches and ethical values.

... the ability to understand, develop and implement the organisation's strategy

royalties and willingness to improve processes, products and services; and

Includes the capacity to lead, manage and co-ordinate.

◾️ Natural capital: all renewable and non-renewable environmental resources and processes that provide goods and services on which the past, present and future success of an organisation is based. Natural capital includes.

Air, water, land, minerals and forests

Biodiversity, ecosystem health.

(Source:International Integrated Reporting Framework Japanese translation)

In addition, with regard to human capital, the Guidelines for Human Capital Visualisation[3] published by the Cabinet Secretariat's Study Group on Visualisation of Non-Financial Information in 2022 provide examples of disclosure items, as shown in the table below.

Table 1 : Human capital disclosure items (Source: Cabinet Secretariat, "Human capital visualisation guidelinesPrepared by the author from)

| field | Examples of disclosure items |

| human resources development | Leadership development skills/experience |

| engagement | engagement |

| liquidity | Recruitment and Retention Succession. |

| diversity | Diversity non-discriminatory parental leave |

| Health & safety | Mental health Physical health Safety |

| labour practices | Labour practices Child labour/forced labour Fairness of wages Relationship with welfare unions |

| Compliance/ethics | Compliance/ethics |

While all of these definitions provide information necessary to measure the value of a company from a perspective that includes sustainability, there are many matters that are difficult to quantify using existing methods or to assume a return in the form of capital. In the following sections, we will look at the regulations and trends in the actual measurement and disclosure of these non-financial capital items.

Human capital-related regulations.

The EU has been ahead of Europe and the US in disclosing human capital and making it mandatory: the EU has required companies with more than 500 employees to disclose information including 'society and employees' in the 'Non-Financial Reporting Directive' (NFRD) since 2014, The scope of application will be extended by the CSRD (Corporate Sustainability Reporting Directive) from 2024 [4].

You can read more about the scope and timing of the CSRD in the following articles

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies | aiESG

In the US, disclosure of human capital-related information became mandatory for all listed companies in November 2020. In addition, in 2021, the Human Capital Investment Disclosure Act was proposed, which would require disclosure of eight human capital items. The bill did not reach a vote in that year, but was reintroduced in September 2023 [5][6].

In Japan, the Cabinet Office Ordinance on Disclosure of Corporate Information [7], promulgated and enforced as of 31 January 2023, makes it mandatory to disclose strategies and targets relating to human capital. Specifically, companies are required to describe their human capital development policy and internal environment development policy in their annual reports, and to indicate measurable indicator targets and progress [8].

Table 2 : Movements towards mandatory human capital disclosure at home and abroad

(Source: Ministry of Economy, Trade and Industry, "Briefing material by the SecretariatPrepared by the author based on "")

| Europe | |

| 2014. | Mandatory disclosure requirements (NFRD), including 'society and employees' |

| 2019 | ISO consolidates indicators on human capital management (ISO 30414). |

| 2021. | Draft revised NFRD published. |

| 2024. | Start of CSRD application |

| United States of America | |

| 2020. | Mandatory disclosure of information on human capital (Regulation S-K amended). |

| 2021. | House of Commons passage of the 'Human Resource Investment Disclosure Act'. |

| 2023. | Reintroduction of the above bill |

| Japan | |

| 2023. | Cabinet Office Order on Disclosure of Corporate Information promulgated and enforced. |

Regulations and guidelines related to natural capital

Regulations and guidelines have been developed for the disclosure of information on natural capital from several perspectives, including resource use and biodiversity.

A particularly noteworthy international initiative is the Taskforce on Nature-related Financial Disclosures (TNFD), which is described in the following article.

[Explanation] What is the TNFD? A new bridge between finance and the natural environment | aiESG

The Natural Capital Protocol[9], developed by the Natural Capital Coalition in 2016 with the aim of including natural capital in corporate decision-making, and the TNFD, a guideline for disclosure purposes, as well as a framework for companies to set their own targets in response to the TNFD. SBTs for Nature, developed as a framework (SBTN blog, first draft 19 Feb - Google Docs) and other references.

With regard to mandatory disclosure of information, in Europe, as with human capital, there are obligations under the ESRS and CSRD, and in 2022, Business for Nature, an international organisation aiming to restore the destruction of nature, announced a request to national governments to require companies to disclose information on their natural capital. announced and signed by more than 400 companies worldwide [10].

In Japan, information disclosure based on the Taskforce on Climate-related Financial Disclosures (TCFD) has become practically mandatory for companies listed on the TSE Prime from FY2022 onwards. This trend towards mandatory disclosure is not limited to climate change, but is likely to expand to natural capital as a whole.

Impact-weighted accounting and the new national wealth index.

So far, we have described some of the major disclosure systems that many countries and companies are currently working on. However, these regulations and guidelines only show the current efforts of individual companies, and it is largely up to investors to read them and make concrete judgments as to how this translates into capital that is linked to the value of the company. This is why the concept of impact-weighted accounts (IWA), which translates a company's impact on the environment and society into monetary units, has begun to attract attention in recent years.

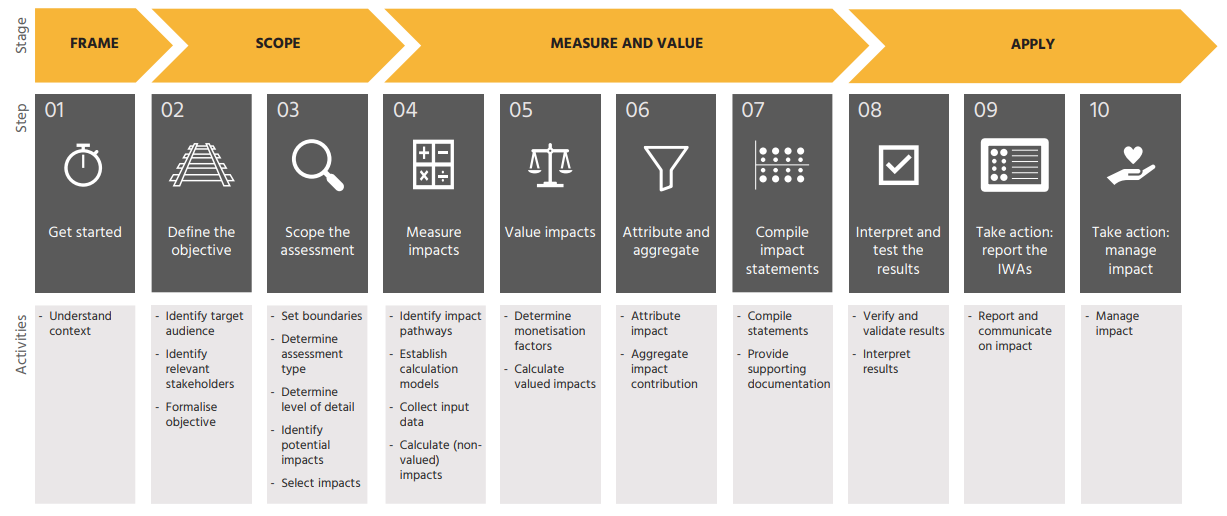

Impact-weighted accounting is being developed by the Harvard Business School and others, and is intended to reflect human and natural capital in a company's income statement and balance sheet by measuring and converting them into monetary values [11]. The Impact-weighted accounts framework (IWAF) published by the Impact Economy Foundation of the Netherlands in 2022 discloses the flow of introducing impact-weighted accounting and some of the coefficients for value conversion [12 12].

Figure 3: Impact-weighted accounts procedure (Source: Impact-weighted accounts framework).

This indicator is groundbreaking in that it allows previously 'non-financial' items such as the natural environment and human capital to be captured continuously with financial information. However, there are some points that need to be kept in mind, such as the fact that the valuation may be highly dependent on the choice of methodology [13].

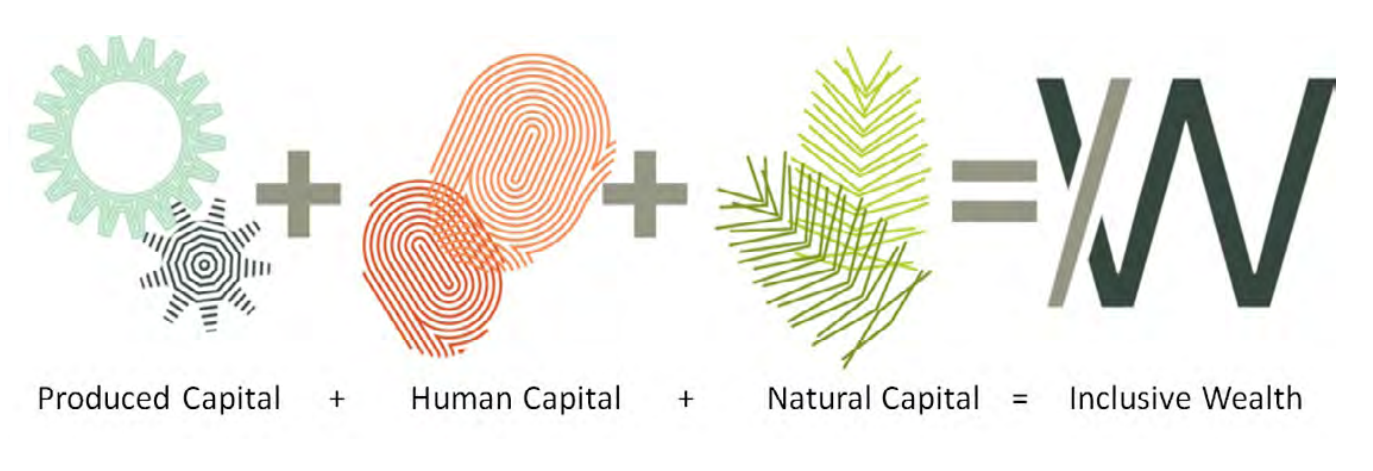

The new Inclusive Wealth Index (IWI), which determines regional wealth, is another attempt to incorporate non-financial information into existing indicators. It is calculated by including the value of all man-made capital (roads, buildings, machinery), human resources (education, health) and natural capital (land, fisheries, climate, mineral resources) and represents the wealth of a country or region instead of GDP (Fig. 4).

Figure 4: Capital comprising IWIs

(Source:Inclusive Wealth Report 2023: Measuring Sustainability and Equity)

The following article explains more about IWI.

Commentary] IWI (New National Wealth Index: Inclusive Wealth Index) - a new indicator to measure wellbeing | aiESG

With the increased focus on human capital and natural capital, it is expected that information disclosure using more objective indicators will be required, in addition to explanations of governance and introduction of corporate initiatives. aiESG enables ESG analysis that goes back to the end of the supply chain, IWI-based analysis and utilisation of natural and human capital management. The aiESG enables companies to approach ESG from a variety of perspectives, including

Conclusion.

This article has focused on non-financial capital, in particular human capital and natural capital, which have become increasingly important in recent years.With the proliferation of ESG-related regulations and frameworks, there is a need not only to focus on obtaining scores, but also to return once again to the perspective of a company's 'capital' and give it back to corporate decision-making and value creation. The focus should not only be on obtaining scores, but also on the company's "capital".

aiESG provides support on everything from basic human capital and natural capital to actual analysis and disclosure. aiESG is happy to assist companies with ESG-related issues.

Enquiry:

https://aiesg.co.jp/contact/

Bibliography

[1] Ministry of Economy, Trade and Industry, 2022

[2] International Integrated Reporting Framework Japanese translation

[3] Cabinet Secretariat, Study Group on Non-financial Information Visualisation, 'TheHuman capital visualisation guidelines'

[4] Ministry of Economy, Trade and Industry, "On the survey on human capital management'

[5] Text - S.1815 - 117th Congress (2021-2022): Workforce Investment Disclosure Act of 2021 | Congress.gov | Library of Congress

[6] Actions - S.2751 - 118th Congress (2023-2024): Workforce Investment Disclosure Act of 2023 | Congress.gov | Library of Congress

[7] Cabinet Office Ordinance amending part of the Cabinet Office Ordinance on Disclosure of Corporate Information, etc.

[8] FSA, "Commentary on the amendments to the Cabinet Office Ordinance on Disclosure of Corporate Information, etc.'

[9] Natural Capital Coalition, "NCPP'

[10] Make it mandatory - EN - Business For Nature

[11] Impact-Weighted-Accounts-Report-2019_preview.pdf (hbs.edu)

[12] The Impact-Weighted Accounts Framework - Impact Economy Foundation

[13] Financial Research Centre, FSA.Current status and prospects for impact-weighted accounting.'

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

Commentary] IWI (New National Wealth Index: Inclusive Wealth Index) - a new indicator to measure wellbeing.

https://aiesg.co.jp/report/240221_iwi/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/

[Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/

[Commentary] TNFD early adopters and their characteristics.

https://aiesg.co.jp/report/240314_tnfd-early-adaptor/

Commentary] Nature Positive : Creating a society that can live in harmony with nature - About OECM and nature symbiosis sites.

https://aiesg.co.jp/report/240214_nature-positive/