Taxonomy is a term referring to a classification system and is used as a classification for sustainable economic activities. Besides the most well-known EU taxonomy, other countries such as ASEAN and China are introducing their own taxonomies.

This article provides an overview of the major taxonomies and a closer look at their impact on Japanese companies.

Greenwash and taxonomy.

As ESG and sustainability become major indicators of economic activity, a growing concern is greenwashing. Greenwash is a combination of the words 'green', which is associated with environmental goodness, and 'whitewash', which means to cheat, and refers to the exaggeration of the real or pretended environmental benefits. In order to prevent evaluations without supporting evidence, there has been a call for the creation of indicators to objectively classify sustainability.

Taxonomies mainly cover business activities and assess what activities of a company contribute to, or do not have a negative impact on, the environment under explicit criteria. Taxonomies do not directly restrict investment in economic activities that are not assessed as sustainable, but they can be used as a basis for investors' decisions, which may result in a disadvantage in terms of financing.

EU Taxonomy.

The most high-profile one is the European Union Taxonomy. The Taxonomy Regulation was developed as part of the Action Plan on Sustainable Finance[1] published in 2018 and has been updated while being progressively applied since its adoption in June 2020. The EU Taxonomy, which was finally approved in 2023, consists of six main environmental objectives and four to be met.

Table 1 : Six environmental objectives and four items (Source:European Commission documentsandMinistry of the Environment dataPrepared by the author from)

| Environmental objectives | |

| Climate change mitigation | Transition to a circular economy |

| Adaptation to climate change | Pollution prevention and control |

| Sustainable use and protection of water and marine resources | Biodiversity and ecosystem protection and restoration |

| Items to be met. | |

| 1. make a substantial contribution to one or more of the six environmental objectives → e.g. improve energy efficiency or protect against pollution | |

| 2. no significant harm to any of the six environmental objectives (DNSH [2]) → no significant carbon dioxide emissions / inefficient use of raw materials, etc. | |

| 3. comply with minimum safety measures → ensure human and other rights at work | |

| 4. meet professional selection criteria (minimum safeguards) → Criteria for meeting 1 and 2 above. Presentation of scientific evidence | |

Specifically, four other environmental objectives have been added to the climate change mitigation and adaptation set out in the first phase. In addition to the uniquely defined categories of green economic activities, reporting is required, including sales from activities that meet the criteria.

The introduction of a 'social taxonomy' has also been considered, with the above-mentioned classification of environmental sustainability being defined as a 'green taxonomy', followed by an assessment of social aspects. This has not been officially updated since the publication of the Final Report [3] in February 2022, but the importance of the social aspects of ESG has been emphasised in the SFDR and CSRD, which are required to be addressed within the EU, and should continue to be closely monitored.

Taxonomy of countries and regions

The movement towards taxonomy setting is not limited to Europe, with various countries and regions setting up their own taxonomies. This chapter covers a number of high-profile taxonomies and looks at their current status and prospects.

ASEAN

ASEAN published the first edition of its own taxonomy in 2021 and updated it to a second edition [4] in 2023. The issues to be considered are very different in South-East Asia, a region with a rapidly growing population and economy, compared to the EU, which is leading the debate on sustainability. All member states participate in the ASEAN Taxonomy Board, the body responsible for reviewing the taxonomy, which provides guiding ideas for countries to develop their own taxonomies. Taxonomies for domestic financial institutions have already been devised in Singapore and Malaysia, where consistency with the ASEAN Taxonomy is also being considered.

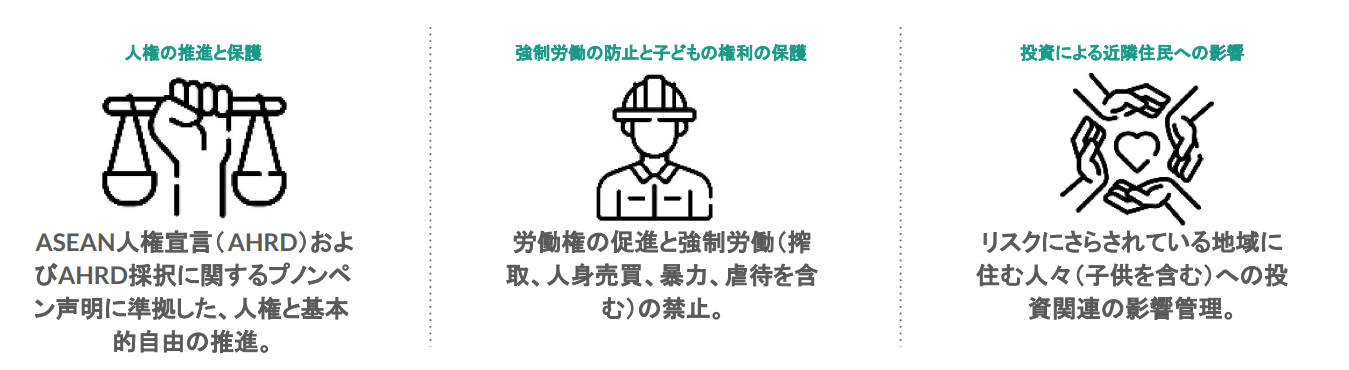

The ASEAN Taxonomy, and the Singapore Taxonomy which has been developed before and after the ASEAN Taxonomy, are characterised by the inclusion of transition concepts, such as the existence of an 'Amber' (yellow) rating, which is an intermediate step towards a 'Green' rating, and a 'Red' rating, which means exit from the market. Taxonomy, but also proposes a unique classification for initiatives in industries with few GHG reduction measures. In addition, the ASEAN Taxonomy presents the minimum Essential Criteria (EC) to be met as 'no significant harm (DNSH)' and 'compensatory measures for transition (RMT)', as well as 'social aspects (SA)' (Figure 1).

Figure 1: Three key social dimensions (SA) (Source:ASEAN Taxonomy documentsPrepared by the author from)

China

In China, the People's Bank of China (PBOC) jointly with the National Development and Reform Commission of China (NDRC) and the China Securities Regulatory Commission (CSRC) published a Chinese version of the taxonomy, the Green Bond Catalogue [5], in 2021. Compliance with this taxonomy is required in order to issue green bonds in China.

A 'white list' of targeted economic activities has been drawn up with a four-level hierarchy starting with six categories, such as energy saving, and a total of 204 programmes indicate specific activities that fit into the taxonomy.

United Kingdom

The UK has decided to introduce its own green taxonomy based on the EU taxonomy, and in the Green Finance Strategy published by the UK Government in March 2023 [6], the UK Government requires voluntary reporting for at least two years after the taxonomy has been finalised, after which, it states that it will consider requiring disclosure. It has also announced its intention to include nuclear power as a green taxonomy investment.

Japan

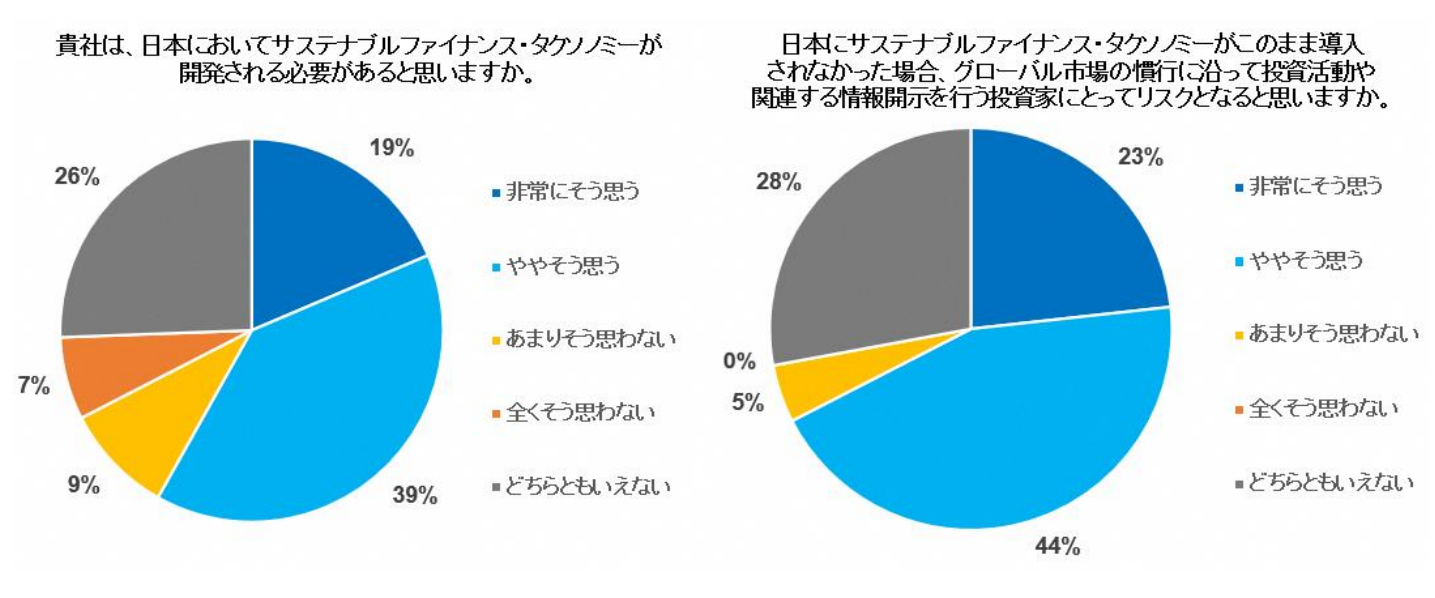

There is currently no taxonomy or plans to introduce one in Japan; in a PRI (Principles for Responsible Investment) 2022 survey of financial institutions investing in the Japanese market, around 60% of respondents supported the development of a sustainable finance taxonomy in Japan (Figure 2).

Figure 1: Opinions on the introduction of a sustainable finance taxonomy in Japan

(Source: PRI 'sThe need for a sustainable finance taxonomy in Japan.")

Impact on Japanese companies

The impact of the introduction of taxonomy in each region on Japanese companies may include the following

1. the impact of EU disclosure requirements

The most direct impact is the EU Taxonomy reporting obligation: large companies based in the EU are subject to the Corporate Sustainability Reporting Directive (CSRD). From 2024 onwards, companies subject to the CSRD will be obliged to report on the compliance of their economic activities with the six environmental objectives of the EU Taxonomy.

The following article explains CSRD in more detail.

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies | aiESG

2.2 Indirect impact 1: Impact of the EU taxonomy

As mentioned above, the EU Taxonomy was established by the European Action Plan, but it may also be used as a standard for companies and investors outside the EU in the future: the emergence of NGOs and ESG assessment bodies using the EU Taxonomy, and the requirement to disclose compliance rates by companies doing business with companies in the target region, could indirectly influence companies not currently covered by the EU Taxonomy. Even companies that are not currently subject to CSRD may be indirectly affected by the EU Taxonomy.

3. indirect impacts➁: other taxonomy impacts

As seen in the previous chapter, a number of non-EU countries and regions have created their own taxonomies. Even though they are not legally binding, it is very costly for companies with global operations to understand the differences in assessments and systems in each region and to consider how to respond. Particularly in regions such as Asia and Latin America, where economic conditions and challenges differ from country to country, the design of systems in each country is also progressing in a disparate manner, so careful handling is required.

Conclusion.

This article provides an overview of the taxonomy, a system for classifying the sustainability of economic activities, its characteristics by country and region, and its impact on domestic companies.The taxonomy started as a sustainability assessment for climate change in the EU, but its scope has tended to expand to other social aspects such as environmental objectives, human rights and forced labour. The scope of the taxonomy tends to expand to include other social aspects such as environmental objectives, human rights and forced labour. There is a small possibility that even companies that are not currently subject to mandatory reporting will have to report taxonomy compliance rates at the request of investment entities or business partners. It is important to start considering as early as possible how your company's economic activities will be classified and what information will be required.

aiESG can provide support from the basic taxonomy to actual disclosure. aiESG encourages companies that need help with ESG compliance to contact us.

Enquiry:

https://aiesg.co.jp/contact/

Bibliography

[1]Sustainable finance: the Commission's Action Plan for a greener and cleaner economy (europa.eu)

[2] "Do No Significant Harm".

[3]Platform on Sustainable Finance's report on social taxonomy (europa.eu)

[4]ASEAN Taxonomy for Sustainable Finance

[5]Green Bond Endorsed Projects Catalogue (2021 Edition)

[6]Green finance strategy - GOV.UK (www.gov.uk)

*Related articles*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/

[Commentary] SFDR: What are the EU Sustainable Finance Disclosure Regulations?

-Obligation to disclose ESG-related information on financial products.

https://aiesg.co.jp/report/2301222_sfdr/

[Commentary] ESRS (European Sustainability Reporting Standard).

https://aiesg.co.jp/report/2301120_csrd/