What is SFDR?

In March 2021, the Sustainable Finance Disclosure Regulation (SFDR) came into force in Europe.

The main objective of the SFDR is to enable investors operating in the European Economic Area to raise funds in a sustainable manner. By disclosing information on the environmental, social and governance ('ESG') aspects of financial instruments to investors in an easy-to-understand manner, the SFDR aims to improve transparency and accountability and prevent greenwashing (i.e. apparent environmental initiatives that are not accompanied by actual actions or activities).

The following table of contents provides details of the SFDR.

Table of Contents

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)Background to the establishment of SFDR

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)What are the main differences between SFDR and EU Taxonomy?

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)SFDR Subject.

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)What is the impact on companies outside the EU, including Japan?

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)Core disclosure requirements

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)Significance of SFDR.

middle dot (typographical symbol used between parallel terms, names in katakana, etc.)Future tasks.

Background to the establishment of SFDR

Prior to the passage of the SFDR, EU financial institutions could set their own standards for ESG disclosure and issue statements. However, there was no means of fact-checking statements in line with these own disclosure standards, which was a problem. The existence of a wide variety of independently set disclosure standards can lead to greenwashing, as financial market participants ('FMPs') and other investors are unable to obtain reliable ESG-related information from the companies they invest in.

For example, some products claiming to be environmentally friendly may not be backed up by legitimate data or other evidence, or human rights may be violated in the manufacturing process of the product. However, if various disclosure standards are in disarray, investors may support companies that are engaged in activities that are not accompanied by the actual situation.

In order to put a stop to these independently set diverse disclosure standards, the SFDR established uniform and clear standards on ESG for financial instruments. The SFDR was then passed in the form of mandatory ESG disclosure for asset managers, FMPs and other investors in the EU.

What are the main differences between SFDR and EU Taxonomy?

To understand the SFDR, it is important to understand how it differs from the EU Taxonomy Regulation ('EU Taxonomy'). While they share the same goal of financing a sustainable society, they have different functions and are designed to complement each other's requirements.

The EU Taxonomy determines whether a company's economic activity is sustainable based on the following six environmental objectives and four conformity requirements.The EU Taxonomy only provides classification and disclosure obligations and does not prohibit investment in economic activities that do not meet the criteria. However, funding for economic activities that are deemed to be unsustainable is considered to be disadvantageous in terms of terms and conditions.

The SFDR, on the other hand, focuses on the disclosure of ESG information on investment products, enabling investors to easily compare information on the sustainability of products. In other words, the EU Taxonomy assesses sustainability based on a company's actual activities, whereas the SFDR focuses on providing information to investors through increased transparency of investment products.

| SFDR | EU Taxonomy. | |

| Subject. | Mainly investment products (e.g. investment funds) | Mainly enterprises and business activities. |

| Objective. | Articulate the sustainability of investment products from an environmental, social and governance (ESG) perspective | Classify sustainable economic activities and identify the environmentally superior activities of companies. |

| means | Require disclosure of ESG information and categorise investment products | Provides a classification system for sustainable economic activities and assesses companies' compliance with the criteria |

| advantage | Make it easier for investors to compare different products | Companies make their own sustainability explicit and increase their credibility to the market |

Table 1 Key differences between SFDR and EU taxonomy

*EU Taxonomy's six environmental objectives and four conformity requirements.

It has a total of six environmental objectives: 1) climate change mitigation, 2) climate change adaptation, 3) sustainable use and conservation of water and marine resources, 4) transition to a circular economy, 5) environmental pollution and pollution prevention and control, and 6) biodiversity and ecosystem protection and restoration.

The four conformity requirements are: a) the activity must substantially contribute to one or more of the six environmental objectives; b) it must not cause significant harm to any of the six environmental objectives (DNSH principle: Do No Significant Harm); c) it must comply with minimum safeguards (including social aspects such as human rights and labour) d) comply with technical screening criteria (principles, indicators and thresholds).

SFDR Subject.

As mentioned above, the SFDR applies to FMPs. It applies primarily to EU-based financial institutions with more than 500 employees, defined as 'big players', as well as banks, insurance companies, investment companies and asset managers; it affects not only financial advisers in the EU but also non-EU-based companies offering products for the EU market. FMPs with less than 500 employees are not obliged to comply with the SFDR. However, Comply or Explain does apply. Parties are obliged to comply with the Corporate Governance Code or, if they do not, to explain why.

The funds affected by SFDR are huge: in 2021, the total assets of EU-based financial companies were EUR 81.6 trillion. And the impact of the SFDR is even greater because it also affects non-EU-based financial companies through their EU subsidiaries. For example, among companies active in the EU financial markets, 62 parent companies with subsidiaries worldwide have a market value of USD 3.2 trillion, of which US companies alone account for USD 2.5 trillion and there are 22.

What is the impact on companies outside the EU, including Japan?

The scope of the SFDR is relatively broad and EU-based FMPs are required to comply. In addition, non-EU FMPs in the US, Asia and other non-EU countries that sell financial products in the EU or provide portfolio management services or investment advice to EU funds are required to comply with the SFDR for each product they sell to EU clients or EU funds they manage or advise.

In other words, even if not directly subject to the disclosure rules, companies that raise funds from European-based financial institutions or investors are affected to a certain extent; non-EU FMPs should consider criteria (i) to (iii) below when determining whether the SFDR disclosure requirements apply to their companies and products. As a general rule, the SFDR applies if any of the criteria (1) to (3) are in the EU. As a result, FMPs in Japan and other countries are also subject to the disclosure obligation.

(i)Location of business units

This is information about where the business unit offering or marketing the financial product or advice is located. For companies and larger entities, different divisions may exist in different locations, such as a parent company, a subsidiary or a branch. If the location of the head office and the location of the relevant branch, for example, is in the EU, the SFDR applies.

(ii) Customer location.

This is information on where the customer (individual or legal entity) purchasing the financial product or advice lives or where they are legally registered. If the customer is located in the EU, the SFDR applies.

(iii) Location of financial instruments, etc.

This is information about where the financial product or advice is registered and where it is offered or marketed. Where a financial product is issued or registered and where it is offered or marketed may be different. Where the financial instrument is issued or offered in the EU, the SFDR applies.

If non-EU companies, including Japanese companies, meet the above criteria, the first thing they should do as a response measure is to collect information for disclosure. Even if economic activities are consistent with the EU taxonomy, it is meaningless if they cannot be disclosed to investors and others due to lack of data. If necessary, data collection and other preparations could be made to enable disclosure.

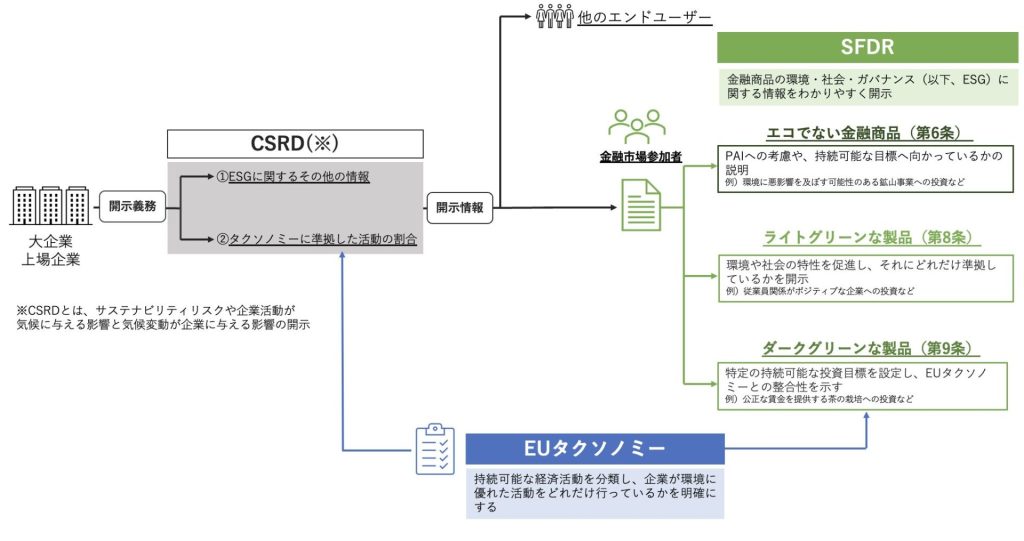

Core disclosure requirements

The SFDR requires two main disclosure requirements, Level 1 and Level 2. Level 1 came into force in March 2021. Level 1 disclosures are at the entity level. Sustainability risk integration policies, adverse sustainability impact events ('PAI') and remuneration policies are required to be disclosed on the financial institution's website Non-EU financial institutions generally tend to be exempt from entity-level disclosure. However, even Japanese financial institutions are required to make entity-level disclosures if they are registered as alternative investment fund managers ('AIFMs') or similar.

Level 2 (Regulatory Technical Standards) was published in April 2022 and came into force on 1 January 2023, complementing Level 1. Level 2 is a financial instrument-level disclosure. Each financial instrument must be classified according to the degree of ESG investment and published in pre-contractual disclosures (pre-contractual disclosure: information on financial products and services is provided to customers before the contract is signed), periodic reports and/or websites.

ESG-related financial products can be broadly divided into two patterns. The first is light green products (Article 8). They must promote environmental and social characteristics and disclose how well they comply with them. This applies to a wide range of financial products, for example, investments in companies with positive employee relations. Second, dark green products (Article 9). Specific sustainable investment targets must be set and alignment with the EU Taxonomy must be demonstrated.

For example, this applies to financial instruments where the objective is sustainable investment, such as investment in the cultivation of tea that provides fair wages. The Article 8 and Article 9 classification of a financial instrument does not require approval, e.g. by a regulator, and is determined by the company itself. As there are no detailed requirements for both classifications, it is not possible to mechanically classify an instrument as Article 8 or Article 9 if certain requirements are met. There are also Article 6 (non-eco financial instruments) that do not meet the criteria for Article 8 or 9. In the case of such products, it must be explained whether the Principal Adverse Impacts on Sustainability (PAI) of the FMP's operational activities have been taken into account and whether they are geared towards sustainable goals. Examples include investments in fossil fuel companies or mining operations that may have negative environmental impacts. Thus, the SFDR requires financial institutions to disclose their sustainability impacts at both the entity and product level.

In addition, in June 2024, the disclosure of Scope 3 greenhouse gas emissions was required. Scope 3 refers to indirect emissions other than Scope 1 and Scope 2 (greenhouse gas emissions of other companies related to the activities of the business). In other words, it refers to emissions upstream (emissions related to purchases) and downstream (emissions related to sales) of a company's activities. Scope 3 has not been standardised in the past, so data has not been developed and it has been difficult to compare comparisons between companies, but there are signs of a gradual move towards standardisation.

Figure 1 Prepared by the author based on FSA (2022).

(in...)https://commission.europa.eu/system/files/2021-04/sustainable-finance-taxonomy-factsheet_en.pdf)

*CSRDis a regulation on the disclosure of sustainability risks and the impact of corporate activities on the climate and the impact of climate change on companies.

Significance of SFDR.

With the introduction of SFDR, FMPs will need to be increasingly attentive to how their investments contribute to global warming, the environment and society, as SFDR requires companies to make a strong case for how well they incorporate environmental and social aspects in their investments, so that financial institutions and advisers will no longer be able to invest in areas that cause serious environmental or social damage or ostensibly take environmental and social considerations into account. It is hoped that these disclosures will encourage everyone from large institutional investors to ordinary investors to choose green investment products, support funds and facilitate the progress towards net zero.

Future tasks.

The SFDR has no restrictions on imports from industries with climate, biodiversity and human rights impacts: in 2022, the EU introduced a new carbon border tariff (novel carbon border tariff) for imports from hard-to-abate industries, such as the steel industry, which have difficulty reducing CO ), but this policy excludes leather produced by deforestation and other examples of negative environmental and social impacts. By focusing only on the European market and stakeholders, important financial flows in the supply chain are missing. While other recent EU policies (e.g. CSRD) have focused on added value and supply chains, the SFDR is still limited with regard to restrictions on products with significant climate change or human rights impacts The SFDR is part of the EU's sustainability policy and future Further policy measures are expected in the future.

aiESG can provide support on everything from basic SFDR to the actual disclosure of non-financial information. aiESG is happy to assist companies that need help in complying with SFDR.

Enquiry:

https://aiesg.co.jp/contact/

References.

https://finance.ec.europa.eu/sustainable-finance/disclosures/sustainability-related-disclosure-financial-services-sector_en

https://www.sustain.life/blog/sfdr-reporting

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/

[Commentary] ESRS (European Sustainability Reporting Standard).

https://aiesg.co.jp/report/2301120_csrd/

[The [ibid.Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/

Commentary] What is the SASB Standard for ESG Information Disclosure? (Part 1) SASB Overview

https://aiesg.co.jp/report/2301025_sasb1/