Materiality (aka material issues) is a crucial concept in corporate reporting, particularly in the context of environmental, social and governance (ESG) investment regulation. It refers to the assessment and reporting of sustainability issues that are considered relevant and influential to a company's financial performance and stakeholder decision-making. There are two main users of this information: investors and stakeholders. By identifying and prioritising these key issues, companies can focus their reporting efforts and address the areas of greatest impact.

This paper aims to briefly summarise materiality, which has been gaining recognition in Japanese companies in recent years, and then categorise the increasingly influential international sustainability reporting standards in terms of the materiality concept (single/double).

1. what is single materiality?

Single materiality is a concept that traditionally refers to information that could reasonably be expected to influence the economic decisions of investors and other users of a company's financial reports. It identifies and reports on sustainability issues that have a material impact on a company's financial performance. The main benefits of single materiality to a company's financial performance are.

... clear focus:

Single Materiality helps companies prioritise their reporting efforts by identifying sustainability issues that have a significant financial impact. This enables effective resource allocation and response to material issues.

... financial risk management:

By considering the financial impact of sustainability issues, companies can better manage and aim to mitigate risks to their financial performance. This can contribute to improved financial stability and resilience.

Investor confidence:

Through single materiality reporting, investors are provided with relevant and meaningful information on sustainability risks and opportunities that could affect the financial performance of a company. This transparency increases investor confidence and attracts sustainable investment.

Compliance with reporting standards:

Many reporting frameworks and standards, such as International Financial Reporting Standards (IFRS) and SASB Standards, still use the Single Materiality as the basis for reporting. By adopting the Single Materiality, companies can ensure compliance with these standards and meet stakeholder expectations.

Although many advantages can be identified as described above, it is possible that single materiality may not capture the wider impacts of a company's activities on society and the environment. Therefore, in recent years, the concept of 'double materiality' has been emerging as an evolutionary version.

2. what is double materiality?

Double materiality is a concept that goes beyond a perspective on the financial impact of sustainability issues on a company and includes a perspective that considers the environmental, social and economic impact of the company's activities themselves. The benefits of double materiality are as follows

... comprehensive report:

Double materiality allows companies to present an overall picture of their sustainability performance by considering both internal (financial) and external (non-financial) impacts. This is expected to improve decision-making and evaluation by stakeholders.

Stakeholder engagement:

Double materiality encourages companies to engage with a wider range of stakeholders, including investors, consumers, business partners and civil society organisations. By involving stakeholders in materiality decisions, companies gain a holistic perspective and build trust and transparency.

... risk management:

By considering the environmental, social and economic impacts of their operations, companies can better identify and manage potential risks and opportunities. This includes understanding the financial implications of sustainability issues and addressing non-financial risks.

Alignment with international standards:

Double materiality is increasingly being adopted in many key sustainability standards, such as the GRI and CSRD (Corporate Sustainability Reporting Directive). By adopting double materiality, companies can ensure consistency with these standards and increase the comparability and consistency of their reporting.

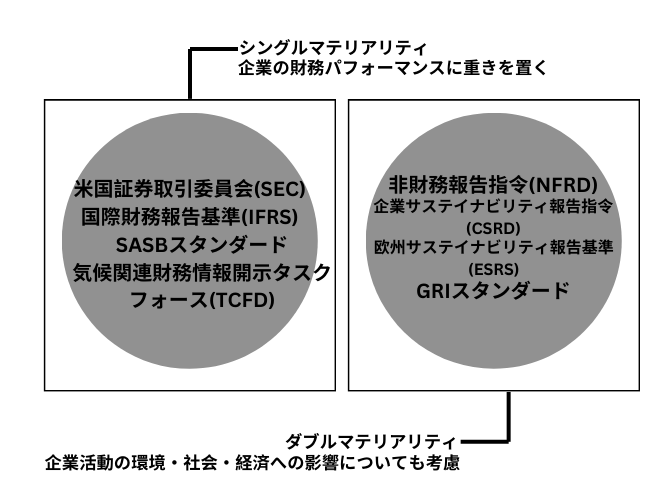

3. which regulations adopt which materialities?

Regulations on sustainability reporting are becoming increasingly diverse in different regions and countries. In such regulations, it is important for companies to check whether single materiality or double materiality is adopted.

Figure 1: Materialisation of typical ESG reporting standards (prepared by the author).

4. summary.

Materiality plays an important role in ESG investment regulation and corporate reporting. Single materiality focuses on the financial impact of sustainability issues, while double materiality has a more comprehensive view by considering both financial and non-financial impacts. Both approaches have advantages and have been adopted in various regulations and standards.

Companies can benefit from a single materiality by focusing on key sustainability issues with high financial impact. On the other hand, a double materiality is expected to provide a more comprehensive view of a company's sustainability performance and improve stakeholder engagement, risk management and alignment with global reporting standards.

Given the global, evolving regulatory focus on double materiality, companies will need to adapt their reporting practices to incorporate both financial materiality and social and environmental materiality. In doing so, companies can increase transparency, attract sustainable investment and meet stakeholder expectations in an increasingly ESG-aware business environment.

aiESG provides support on ESG-related standards and frameworks, from basic content to actual disclosure of non-financial information. aiESG is happy to assist companies with ESG compliance.

Enquiry:

https://aiesg.co.jp/contact/

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

[Commentary] Alphabet soup - Disorder and convergence of sustainability standards.

https://aiesg.co.jp/report/2301226_alphabet-soup/

[The [ibid.Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/

Commentary] What is the SASB Standard for ESG Information Disclosure? (Part 1) SASB Overview

https://aiesg.co.jp/report/2301025_sasb1/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/