Introduction.

In recent years, there has been a spread of global social issues that we all need to solve together, such as the intensification and frequency of natural disasters around the world caused by global warming, and human rights abuses such as child labour and forced labour in overseas supply chains. ESG issues therefore represent challenges that need to be solved by various organisations, such as companies, in order to achieve the same goal and achieve a sustainable society. In order to solve these challenges, the Sustainable Development Goals (SDGs) and the Paris Agreement have been adopted, and a shift towards new industrial and social structures for a sustainable society is underway.

However, achieving a sustainable society requires huge amounts of public and private sector funds for capital investment and technological development. Therefore, sustainability initiatives are also becoming indispensable in the financial sector. Financial institutions need to look at sustainability issues from the perspective of portfolio risk management, taking into account not only greenhouse gas emissions reductions from their own business activities, but also emissions from their trading partners and supply chains.

In recognition of this, sustainable finance is spreading rapidly. For example, according to bloomberg, ESG (environmental, social and governance) investment balances are expected to reach USD 53 trillion by the end of 2025, up from USD 37.8 trillion at present ESG assets under management will account for more than a third of the total USD 140.5 trillion expected to be under management by 2025. of the total USD 140.5 trillion expected to be under management by 2025. Thus, the global ESG (environmental, social and governance) asset base continues to grow. Furthermore, the COVID-19 pandemic in 2020 has further increased interest in sustainable finance ('sustainable finance').

With the growing interest in sustainable finance, this article looks at how the financial industry has responded to the growing interest in sustainable societies.

What is sustainable finance?

The Principles for Responsible Investment (PRI), proposed by then UN Secretary-General Kofi Annan in April 2006, are an initiative to promote the flow of funds to address ESG issues through investment. It became an international trend when major institutional investors in Europe and the USA signed up to it.

The PRI requires institutional investors and others to take a long-term perspective when analysing and evaluating companies and to take ESG information into account in their investment behaviour.The Paribas Shock (August 2007) and Lehman Shock (September 2008), which followed the PRI's advocacy, are said to have motivated the spread of the PRI with an ESG focus. The PRI is said to have been a motivation for the spread of ESG-focussed PRIs. In addition, the SDGs, adopted by agreement of all 193 Member States at the UN General Assembly in September 2015, and the Paris Agreement, adopted at COP21 (21st session of the Conference of the Parties) in November 2015, have further spread interest in ESGs.

Thus, sustainable finance refers to financial approaches and initiatives that promote the resolution of social issues through loans and investments, taking into account not only the interests of companies but also ESG perspectives. Sustainable finance is said to consist mainly of two approaches: (i) ESG investment, in which institutional investors invest in listed companies, and (ii) ESG financing, in which financial institutions lend to companies.

However, according to the Financial Services Agency's June 2021 report, Building a Financial System to Support a Sustainable Society, sustainable finance is not a specific financial instrument, but rather broad and refers to a whole range of financial mechanisms, codes of conduct and evaluation methods to build a sustainable society. Below, we look at sustainable finance in its broadest sense, in addition to the process of investing in and financing projects to build a sustainable society.

What is ESG investment and financing?

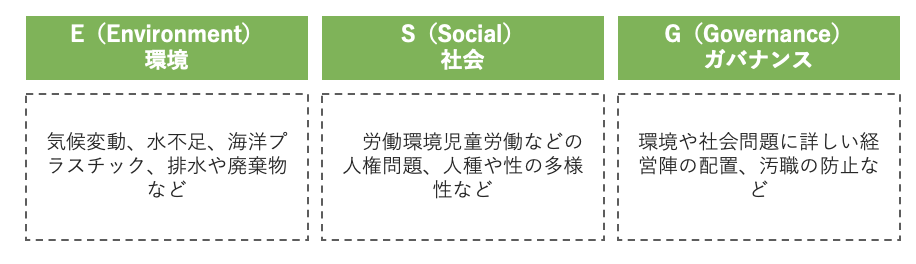

ESG is an acronym for Environment, Social and Governance. More specifically, ESG encompasses the issues listed in Figure 1 below. Investing and financing companies based on how they address these issues is called ESG investment and financing. In other words, ESG financing investment is an initiative by institutional investors and financial institutions to consider and mitigate social issues through loans and investments in companies and other entities.

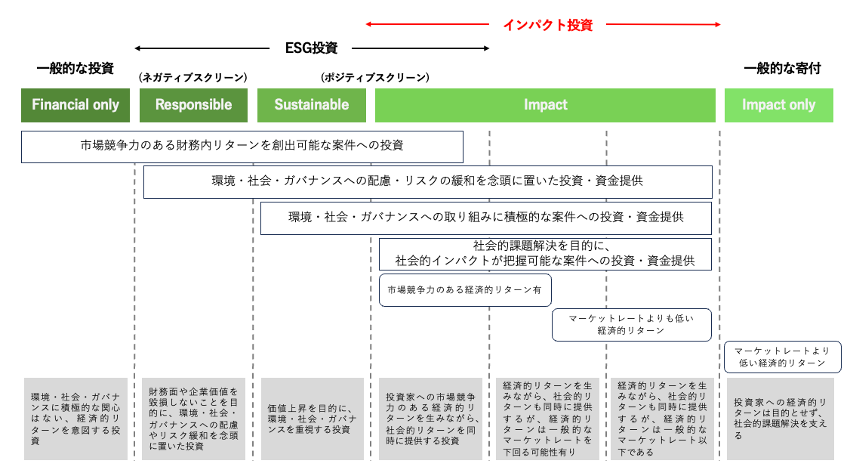

The third report of the FSA's Expert Group on Sustainable Finance has made a particularly strong statement of its own in the area of impact investment, which aims to balance profitability with solutions to environmental and social issues. Impact investment and ESG investment may seem similar, but what exactly are the differences? We look at the differences between impact investment and ESG investment in comparison with other approaches, including general investment.

Impact investing and ESG investing have in common that they both aim to contribute to social issues, but ESG investing incorporates environmental, social and governance perspectives, but primarily considers ESG in the management of companies and in investments. Impact investing, on the other hand, seeks economic benefits as well as social returns and evaluates the results quantitatively and qualitatively. In other words, ESG investment focuses on the sustainable management of a company, whereas impact investment emphasises and assesses direct social change. It should be noted, however, that ESG investment and impact investment in general include a wide variety of investment styles. A detailed categorisation of investment styles is shown in Figure 1.

Source:https://impactinvestment.jp/user/media/resources-pdf/impact_investment_report_2019.pdf

The whole picture of finance for building a sustainable society.

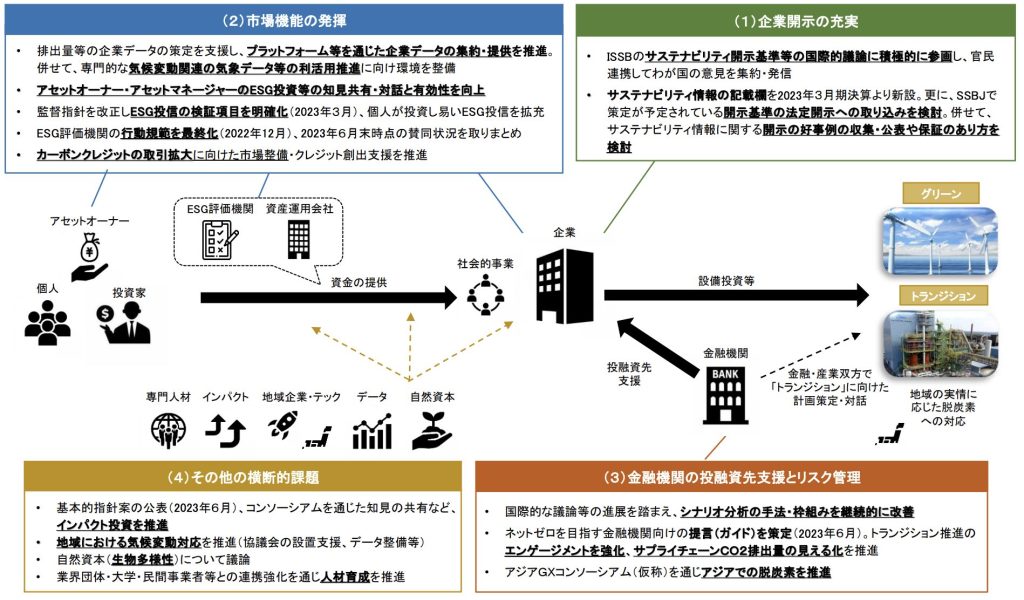

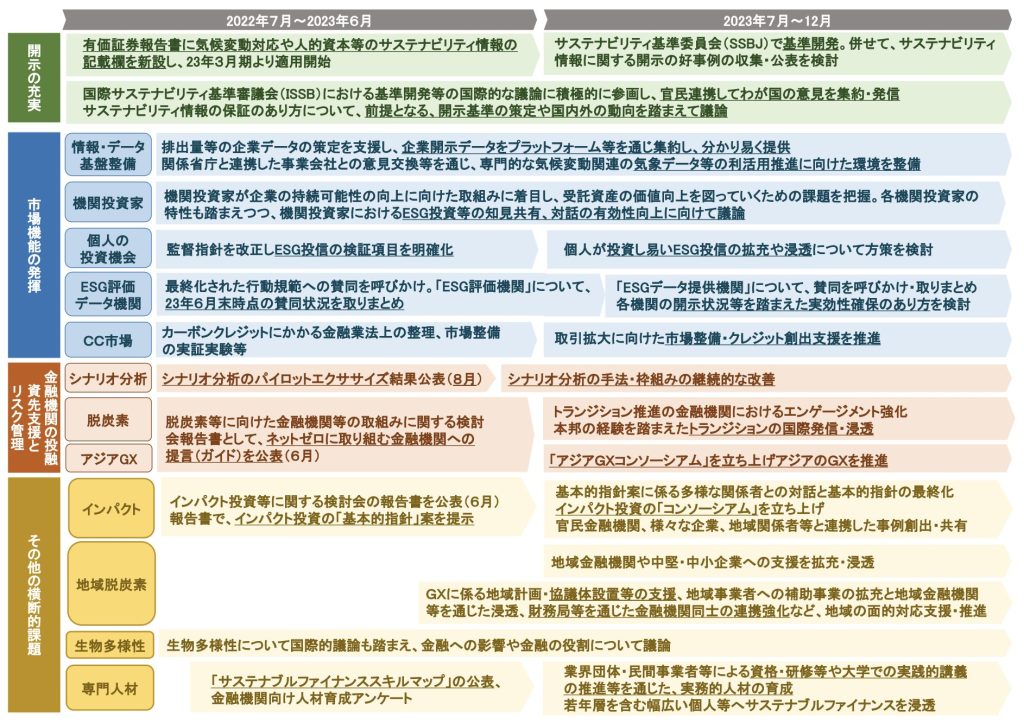

In December 2020, the FSA established the Expert Group on Sustainable Finance to position sustainable finance as an infrastructure that supports a sustainable economic and social system; in June 2023, while maintaining the main pillars of the measures, it assessed emerging issues and recognised points of contention and developed an overall picture of the challenges and implementation of the measures. The report recognises that sustainable finance initiatives in Japan have made progress and that institutional arrangements have been developed in each of the measures. In this issue, we will look briefly at the overall picture of sustainable finance in Japan, focusing on four points of particular importance among the progress and challenges of sustainable finance initiatives listed in the third periodic report.

(1) Enhancement of corporate disclosure

The International Sustainability Standards Board (ISSB) at the IFRS Foundation finalised the general disclosure requirements (S1 standard) and the climate-related disclosure standard (S2 standard) in June 2023. The International Auditing and Assurance Standards Board (IAASB) is also about to finalise in September 2024 the assurance practices that auditors have in place to ensure the reliability of sustainability information.

(2) Market functions.

The report summarises past efforts and future challenges and directions for action with regard to the development of information and data infrastructures, the provision of investment opportunities to institutional investors and individuals, ESG assessment and data providers, and the carbon credit market. In the area of carbon credit trading, as efforts to meet international decarbonisation targets progress, there is an increasing number of requests for companies to procure credits on the market for reductions not yet achieved. In Japan, similar requests have been made to GX League companies, and with the planned pilot introduction of growth-oriented carbon pricing from 2026, demand for carbon credit trading is expected to grow. The financial sector is expected to contribute in various ways, such as brokering carbon credit transactions and creating new market transactions. The Tokyo Stock Exchange will also open a carbon credit market in 2023, and the Financial Services Agency is working on legislation. The private sector is expected to develop and promote practical projects that contribute to carbon absorption and reduction, and it is important to create a high-quality market through public-private partnerships.

(3) Financial institutions' support for investment and loan recipients and risk management.

Status of risk management, including scenario analysis.

With regard to scenario analysis, which was identified as an effective method in the Basic Approach to Addressing Climate Change in Financial Institutions published in July 2022, the Financial Services Agency (FSA) and the Bank of Japan (BOJ) conducted a pilot climate-related scenario analysis using the scenarios published by the Network of Financial Authorities on Climate Change Risks (NGFS) as common scenarios. The FSA and the BOJ conducted a pilot project on climate-related scenario analysis using the scenarios published by the Network of Financial Authorities on Climate Change Risks (NGFS) as common scenarios. The results of the analysis and the main issues and challenges were published in August of the same year.

Initiatives by financial institutions and others towards decarbonisation, etc.

In order to promote effective dialogue between financial institutions and companies, a study group was set up in October 2022 on the approaches of financial institutions towards decarbonisation, etc., and a report was published in June 2011. The report provides recommendations on issues that financial institutions should consider, including specific measures.

Expanding GX Finance in Asia

Transition investments in Asia could be implemented by utilising Japan's financial functions, leading to the creation of an international trading hub (Asian GX financial hub), etc.

(4) Other cross-cutting issues.

Promoting impact investment

Impact investing has the same significance as sustainable finance in general in that it contributes to solving social and environmental issues through investment and improves the sustainability of investments and corporate activities in general by appropriately incorporating externalities into financial markets. In particular, there is a high affinity with, and high expectations for, support for start-ups and other companies that aim to balance business viability with the resolution of pressing issues.

Climate change response in the region

Decarbonising SMEs, which account for 1-20% of greenhouse gas emissions (Scope 1), is crucial to achieving carbon neutrality. However, while addressing climate change is envisaged to have a range of benefits for local SMEs, they need to address an extremely wide variety of key management issues in parallel with a limited number of staff. While recognising the importance of climate change responses, initiatives may be hampered by a lack of human, information and financial resources. On the financial side, it is expected that regional financial institutions with close ties to local companies, in cooperation with the national government, local authorities, Keidanren and others, will provide consulting services such as emissions measurement and energy-saving support.

Debate on natural capital and biodiversity and future prospects.

Accurate assessment of impacts on ecosystems is difficult and data development is a challenge. In particular, biodiversity has not been well assessed, making it difficult for companies to measure their impact. In the future, the quality of ESG data is expected to improve and risk analyses on biodiversity to be developed, so that companies can formulate concrete environmental strategies.

human resources development

A side effect of the progress of the initiative is the apparent shortage of human resources. Comprehensive cross-sectoral initiatives are important. The FSA has developed a skills map to promote the development and retention of human resources.

Source:https://www.fsa.go.jp/policy/sustainable-finance/report_ja.pdf

Codes of conduct and assessment methods for achieving a sustainable society.

Finally, we look at the differences between the ICMA Principles and the PIF Principles, which have attracted particular attention recently in terms of codes of conduct, assessment methods, etc. for building a sustainable society.

What is ICMA?

The International Capital Markets Association (ICMA) plays a key role in the development of international principles for ESG finance; ICMA has a mission to promote the healthy development of international bond markets through market transparency, disclosure and reporting and develops voluntary guidelines and public relations activities.

In this context, various guidelines were published in January 2014, including the Green Bond Principles. Subsequently, the Social Bond Principles (June 2017), the Sustainability Linked Bond Principles (June 2020) and the Climate Transition Finance Handbook (December 2020) were added, and these principles are regularly revised. Recent revisions have highlighted the Framework and External Assessment in particular as key recommendations. External assessment refers to the process by which an issuer appoints an external assessment body and confirms conformity through its assessment.

In ESG finance practice, issuers develop a framework based on ICMA principles and national guidelines, which is then assessed by an evaluation company to provide an external evaluation. The national guidelines, while compliant with the ICMA Principles, take into account national circumstances and specific examples of responses. However, it can be difficult to fully assess a company's sustainability based on ICMA alone. Companies can complement the ICMA Principles by complying with the Positive Impact Financing (PIF) Principles, which assess comprehensive initiatives, to develop a framework that enables financing based on sustainability strategies. For example, the Green Bond Principles select the use of funds based on business segmentation, which means that the assessment of impact is limited to a limited number of business areas.

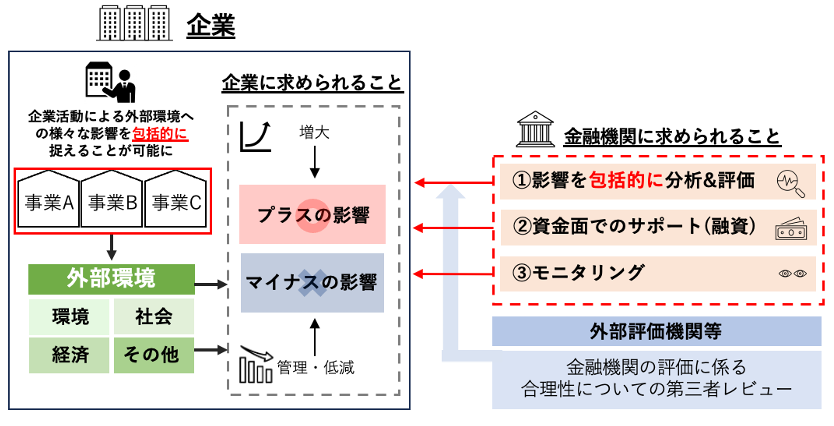

What is positive impact finance (PIF)?

The United Nations Environment Programme and Finance Initiative (UNEP FI) Positive Impact Finance (PIF), developed in January 2017, aims to help companies develop activities to achieve a sustainable society, which are then reviewed, evaluated and promoted by financial institutions and others. The framework identifies and assesses the positive impact of a company's activities and then provides support, such as loans, and monitors its operations The PIF principles comprise four principles, which are: a) the positive impact of the company's activities on the environment, b) the positive impact of the company's activities on the environment and c) the positive impact of the company's activities on the environment.

Principle 1 is that positive outcomes can be identified for the three pillars (environmental, social and economic) contributing to the SDGs and that negative impacts are identified and addressed; Principle 2 is that an evaluation framework, including adequate processes, methods and evaluation tools, is developed for PIF implementation; Principle 3 is that projects and other measures of positive projects and other details, evaluation and monitoring processes and transparency on positive impacts; Principle 4 is that PIF instruments are evaluated by an internal organisation or a third party.

In other words, the PIF Principles take a comprehensive view of a company's efforts towards sustainability, with reference to its key issues. It selects and funds projects that expand the positive aspects or curb the negative aspects of the key issues to achieve the company's goals. By looking at the company's own Key Performance Indicators (KPIs), investors can easily determine whether the company is capable of sustainable growth.

Prepared by the author based on Sumitomo Mitsui Trust Bank's Positive Impact Finance.

Source:https://www.smth.jp/sustainability/Initiatives_achievements/pif

aiESG provides support on ESG-related standards and frameworks, from basic content to actual disclosure of non-financial information. aiESG is happy to assist companies with ESG compliance.

Enquiry:

https://aiesg.co.jp/contact/

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

[Commentary] Alphabet soup - Disorder and convergence of sustainability standards.

https://aiesg.co.jp/report/2301226_alphabet-soup/

[Commentary] SFDR: What are the EU Sustainable Finance Disclosure Regulations?

-Obligation to disclose ESG-related information on financial products.

https://aiesg.co.jp/report/2301222_sfdr/

[The [ibid.Explanation] What is the TNFD? A new bridge between finance and the natural environment

https://aiesg.co.jp/report/230913_tnfdreport/

Commentary] What is the SASB Standard for ESG Information Disclosure? (Part 1) SASB Overview

https://aiesg.co.jp/report/2301025_sasb1/

Commentary] CSRD: The EU version of the Sustainability Reporting Standard just before it comes into force - the impact on Japanese companies.

https://aiesg.co.jp/report/2301120_csrd/