In recent years, the sustainability of corporate activities has become more and more important and more companies are disclosing non-financial information with reference to ESG-related international standards and other standards. But how is this vast amount of information being captured and reflected in actual investment? In this issue, we focus on the current state of international 'sustainable investment' and the challenges it faces.

Table of contents:

Seven methods of sustainable investment.

Current status of sustainable investment

Issues surrounding sustainable investment and ESG management

Effort to disclose information

Deviation from the actual situation

Difficulties in evaluation

Conclusion.

Seven methods of sustainable investment.

What type of investment does sustainable investment refer to in the first place? Terms such as sustainable investment, impact investment and ESG investment are used rather vaguely and it is often difficult to clearly explain the differences between them.

In this article, the discussion is based on the seven methods defined by the Global Sustainable Investment Alliance (GSIA), an international organisation promoting sustainable investment.

| technique | Overview. |

| impact investment | Investment for positive social and environmental impact Measurement and reporting of impact and proof of investor intent is required. |

| Positive/best-in-class screening | Investments in sectors, companies and projects that demonstrate good and above specified threshold ESG performance within the industry |

| Sustainability and thematic investment | Investment in themes and assets that contribute to sustainable environmental and social solutions (e.g. sustainable agriculture, gender equality). |

| Code-based screening. | Screening according to compliance with international norms, such as standards issued by the UN, ILO and OECD. |

| negative screening | Exclusion of certain sectors, companies, countries, etc. from funds or portfolios, depending on the products or business activities that are deemed not to be investment-eligible (e.g. arms manufacturing, animal testing). |

| ESG integration | An investment approach that systematically and explicitly incorporates environmental, social and governance factors into financial analysis with the aim of improving risk-adjusted returns. |

| Corporate engagement and voting rights | Using investors' rights to influence corporate behaviour through communication with management and voting rights |

Table 1 : Sustainable investment instruments

(Source:Definitions for Responsible Investment ApproachesPrepared by the author from [1])

Non-financial information disclosed by companies can be used in a number of ways, including when it is used to compare companies with their peers (positive/best-in-class screening), when compliance with codes is checked (code-based screening) and when initiatives are evaluated in various ways (e.g. sustainability theme investment). There are A combination of these methods is used in actual investment products and investment strategies, with the proportion of these methods showing a trend that varies from region to region and year to year.

Current status of sustainable investment

Although the growing focus on sustainable investment would seem to indicate that investment balances are increasing globally, this is not necessarily the case. The graph shows sustainable investment balances for each country and region according to the Global Sustainable Investment Review published by the GSIA.

Figure 1: Sustainable investment balances

(Source:Global Sustainable Investment Review 2022Prepared by the author from)

The figure shows a marked decline in the US data between 2020 and 2022. This reflects a change in survey methodology, with many ESG integrations no longer being counted, which had accounted for the majority of US sustainable investments until the 2020 survey. While it is possible to attribute this result simply to the change in standards, it is also possible that products with ambiguous realities may have been treated as sustainable investments in the past. The fact that different countries and regions have different evaluation bodies also complicates the overall picture.

Meanwhile, the balance of investment in Japan has been growing consistently. According to a survey by the Japan Sustainable Investment Forum (JSIF), the total value of sustainable investment exceeded 537 trillion yen at the end of March 2023 [2].

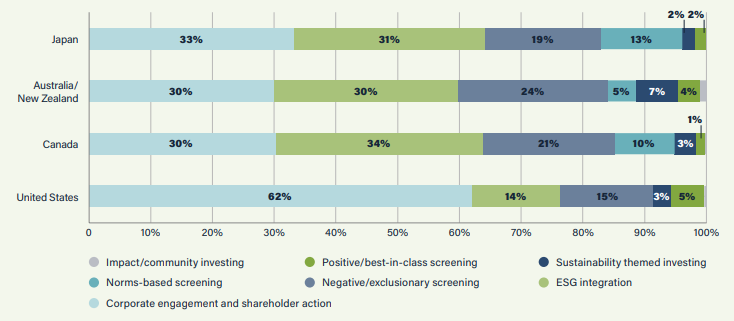

Differences between countries can also be seen in the breakdown of sustainable investment. Figure 2 shows the percentage of sustainable investment by method in Japan, Australia/New Zealand, Canada and the USA.

Figure 2: Breakdown of sustainable investment in different countries

(Source:Global Sustainable Investment Review 2022)

The investment breakdown for Europe is not disclosed in this GSIA report. In the other countries and regions, corporate engagement/voting, ESG integration and negative screening account for more than 80% of the total. In Japan, negative screening accounts for a relatively small proportion and norm-based screening is also the method of choice.

The US shows a distinctive graph of 621 TP3T for Corporate Engagement and Voting, which is due to the exclusion of funds that did not include specific information on ESG integration due to the aforementioned change in survey methodology.

The concept of sustainability can no longer be ignored in the marketplace, but even at present, the evaluation and use of ESG scores varies. While the trend towards companies being required to disclose non-financial information is expected to continue, it is likely that companies will take a harsher view of information with ambiguous evaluation criteria and the potential for greenwashing.

Issues surrounding sustainable investment and ESG management

This section now looks at the challenges for corporate ESG management and its assessment systems. The following hurdles exist for companies engaging in information disclosure and for investment entities investing in sustainability

Effort to disclose information

First, corporate ESG information disclosure involves many costs. Just organising the necessary information is no easy task, given the barrage of disclosure standards set by international organisations and others, the variety of disclosure items required, and the huge amount of data to be processed. The path to getting the information together is not limited to information that can be completed in-house, such as the percentage of women in management positions, or items that are easy to visualise and measure quantitatively, such as carbon dioxide emissions, but also includes items for which there are no clearly established disclosure standards, such as items that require data back through the supply chain, or items with a social dimension. The path to having all this information in place varies. Furthermore, ESG itself covers many fields and requires a wide range of skills, including the use of systems for data analysis and scrutiny of international standards, making it a challenge for companies in general to find the right people to take charge.

Deviation from the actual situation

ESG information disclosure is associated with various difficulties, but it has also been pointed out that there is a discrepancy between the actual information that is actually published and the actual business. In addition, even if data is collected, if it cannot be used to improve operations, it will not lead to increased corporate sustainability: according to a survey of Japanese companies in 2023, more than 55% of companies said they were unable to utilise the ESG data they had collected for management decision-making and business operations. [3]. Some say that it is necessary to raise awareness not only among senior management, but also among employees as a whole regarding corporate initiatives, and methods such as linking remuneration to ESG scores are being implemented in companies around the world [4].

Difficulties in evaluation

Due to the above-mentioned ESG management challenges, it is still not easy for investment entities to evaluate companies using non-financial information. In addition, the state of affairs has not yet reached a point where companies reluctant to contribute to ESG are forced to exit the market, as investors differ in their evaluation criteria and the priority given to ESG items. Investors and markets are increasingly calling for greater transparency and greenwashing measures from ESG assessment bodies, as well as establishing an investment perspective in sustainable investment, which requires a long-term perspective before returns can be achieved.

Conclusion.

In this article, we have focused on the current state of sustainable investment and the challenges of ESG management in the context of the corporate and market sustainability movement: there is a need to go beyond research and initiatives for ESG reporting, to understand the current situation, to improve the actual situation and to create a framework for investment from a long-term perspective.

aiESG provides support on everything from the basics of sustainable investment and ESG management to the actual disclosure of non-financial information. aiESG is happy to assist companies with ESG-related issues.

Enquiry:

https://aiesg.co.jp/contact/

Bibliography

[1] Definitions for Responsible Investment Approaches (gsi-alliance.org)

[2] JSIF Survey 2023 Results Release Bulletin.pdf (japansif.com)

[3] Survey 2023 on ESG data collection and disclosure

[4] Survey of global management and investor attitudes to 'ESG' and 'remuneration' (pwc.com)

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

Commentary] Sustainable finance.

~Sustainable Response in the Financial Industry ~.

https://aiesg.co.jp/report/240209_sustainable-finance/

[Commentary] SFDR: What are the EU Sustainable Finance Disclosure Regulations?

-Obligation to disclose ESG-related information on financial products.

https://aiesg.co.jp/report/2301222_sfdr/

[Paper commentary] The relationship between environmental assessment and stock returns.

~ Investors regard companies that do not engage in environmental management as a significant risk ~.

https://aiesg.co.jp/report/230712_escore_investor/

[Commentary] Alphabet soup.

〜˜ Turbulence and convergence of sustainability standards ˜.

https://aiesg.co.jp/report/2301226_alphabet-soup/