An integrated report is a document in which a company comprehensively reports on the organisation's value creation processes, including not only financial information but also non-financial information such as environmental, social and governance (ESG).

The main objective of an integrated report is to provide investors and multi-stakeholder groups with a better understanding of a company's sustainability and long-term performance.

In this article, we would like to inform you about the current status and latest developments in integrated reporting in Japan.

Current status of integrated reporting in Japan.

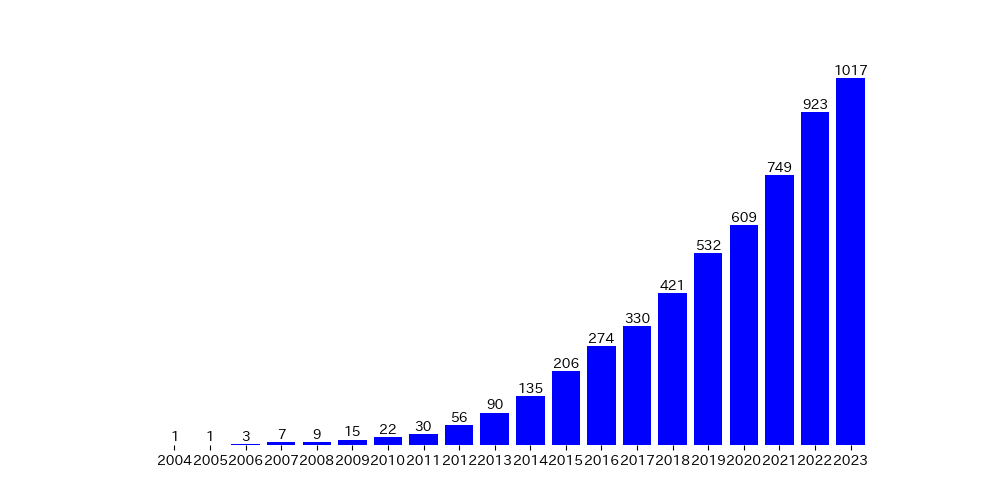

According to a study by Edge International, the number of companies issuing integrated reports in 2023 is 1017, approximately 1.1 times the number of companies last year. The number of companies issuing such reports has been increasing rapidly, especially in recent years.

Figure 1: Number of companies and other entities issuing domestic self-reported integrated reports

(Edge International, "Trends in integrated reporting to support sustainable growth in Japan 2023.(Prepared by the author from 'The author.)

As the number of issuing companies increases, so does the content.

One example of this is the marked increase in the number of companies incorporating materiality, one of the key concepts in sustainability reporting, into their integrated reports.

Materiality on corporate value, which is the focus of investors, and materiality on the environment and society, which is the focus of multistakeholders, have both seen an increase in the rate of disclosure in integrated reports.

There is growing recognition that materiality disclosure is an essential element of the integrated report, and a large proportion of companies issuing an integrated report for the first time now also disclose materiality.

| disclosure element | 2021 (%) | 2022 (%) |

| Disclose materiality from a corporate value perspective. | 43.8 | 65.6 |

| Disclosure of materiality from an environmental and social perspective. | 57.5 | 70.1 |

Table 1: Materiality 1 of the Integrated Report

(Edge International, "Integrated Report 2022 Survey - Materiality.(Prepared by the author from 'The author.)

Issues in integrated reporting in Japan.

On the other hand, challenges remain in integrated reporting.

For example, all companies mention human rights in their integrated reports. However, only a few disclosures delve deeply into the assessment of human rights risks, which is useful for investors and multi-stakeholder groups. Investors expect a specific description of the possible risks and how to deal with the risks they face.

Other indicators and targets, such as quantitative information on, for example, the number of human rights due diligence (human rights DD) issues that have been raised, could also be disclosed to promote investor understanding. In many cases, disclosure responses to materialities other than human rights are only introductory and do not go into specific details.

| Contents | Disclosed (%) | No disclosure (%) |

| SASB Reference. | 19 | 81 |

| Analysis of current situation vis-à-vis market valuation. | 30 | 70 |

| Business portfolio management | 59 | 41 |

| Investment allocation areas | 57 | 43 |

| Understanding the cost of capital | 39 | 61 |

| Risk response measures. | 36 | 64 |

| TCFD scenario analysis | 74 | 26 |

| Risks, opportunities and impacts of natural capital | 32 | 68 |

| Link between human resources strategy and management strategy. | 68 | 32 |

| Assessment of human rights risks | 26 | 74 |

| Corporate Value Materiality | 86 | 14 |

| Materiality KPIs. | 63 | 37 |

| intellectual property | 48 | 52 |

| DX | 67 | 33 |

| Activities of the Sustainability Committee and other committees | 51 | 49 |

| Activities of the Board of Directors | 64 | 36 |

| Skill sets and management strategies | 35 | 65 |

| Status of dialogue with shareholders and investors. | 71 | 29 |

Table 2: Materiality 2 of the Integrated Report

(Edge International, "Creating Corporate Value through Integrated Reporting - The State of Integrated Reporting in Japan 2023 -.(Prepared by the author from 'The author.)

While more companies are publishing integrated reports, the lack of a standardised framework in Japan has resulted in variations in the quality and scope of reporting between companies.

Necessity of English-language disclosure.

And a recent hot topic with regard to integrated reports and other disclosures is disclosure in English.

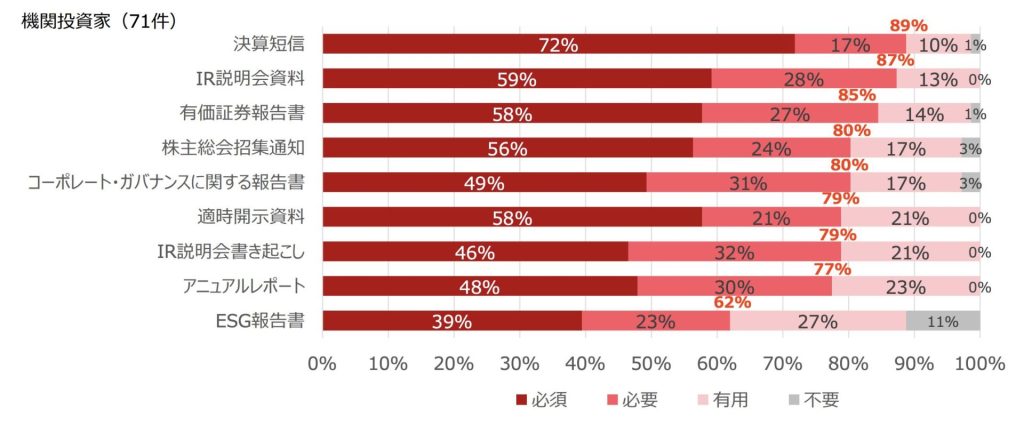

From March 2025, the Tokyo Stock Exchange will require companies listed on the prime market to disclose material information in English as well as Japanese. Overseas investors use materials disclosed by companies in English as their main source of information when making investment decisions. Therefore, the publication of English-language versions of materials increases the likelihood of receiving investment from Japanese as well as foreign investors.

However, foreign investors are not satisfied with the current English disclosures. There are two main reasons for this.

The first is that it is not disclosed in English in the first place, or even if it is disclosed in English, it contains less information than the Japanese version.

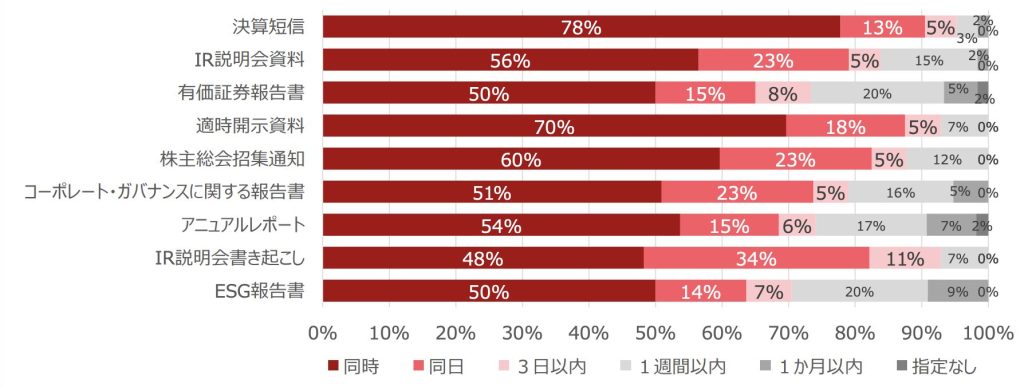

Figure 2-1: Materials requiring disclosure in English

(Source: JPX) Results of a questionnaire survey of foreign investors on English-language disclosure (summary version).)

Figure 2-2: Scope of prime market English language disclosure

(Source: JPX) English Disclosure Implementation Survey Aggregate Report.)

Most foreign investors require or require that all documents are disclosed in English.

However, at most 60% of them disclose everything in English, indicating that they do not meet the demand of foreign investors.

The second reason is that disclosure in the English version is slower than in the Japanese version.

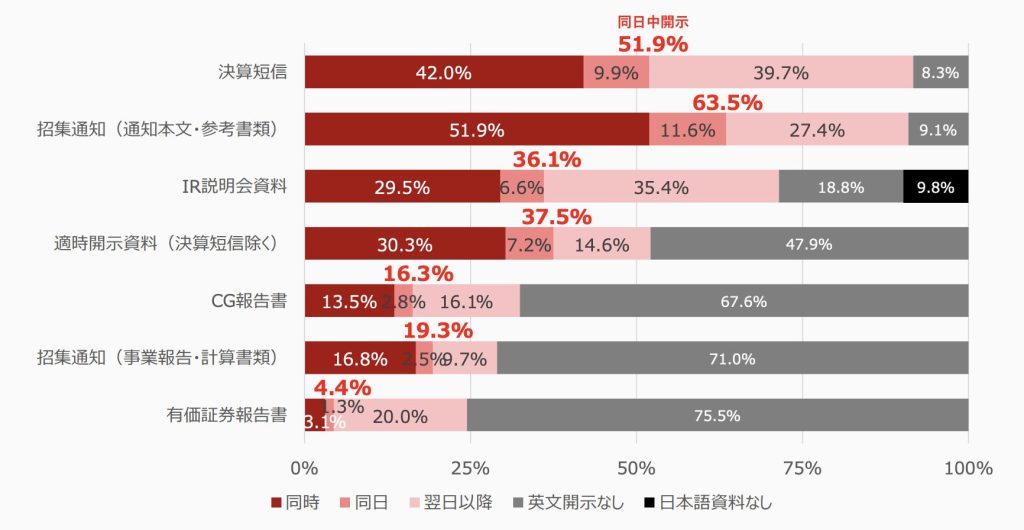

Figure 3-1: When English disclosure is required

(Source: JPX) Results of a questionnaire survey of foreign investors on English-language disclosure (summary version).)

Figure 3-2: Prime market Timing of English disclosure

(Source: JPX) English Disclosure Implementation Survey Aggregate Report.)

While many foreign investors are requesting disclosure on the same day, many are disclosing their information on the following day or later. This also shows that they are not able to meet investors' expectations.

Insufficient English disclosure makes it difficult for overseas investors to obtain real-time information and puts them at a disadvantage compared to Japanese investors. As a result, overseas investors will not be able to secure sufficient time to make investment decisions, which may lead to withdrawal from investment in many cases.

Conclusion.

Integrated reporting has become increasingly important in recent years in response to growing interest in ESG.

In order to provide a better understanding of a company's sustainability and long-term performance, it is important to refine the content of the integrated report and clearly communicate the company's sustainable value creation process.

Furthermore, more accurate and prompt English-language disclosure is also more appealing to foreign investors. English-language disclosure is essential for expanding the global investor base.

aiESG uses the generative AI developed by us.aiESG for IR, an integrated report evaluation service.The company provides the following services. This service determines the consistency between ESG-related social demands and the integrated report of the company being assessed, and scores it objectively on multiple items. Companies that have problems with their integrated reports are welcome to contact us.

Enquiry:

https://aiesg.co.jp/contact/

Reference.

Corporate Value Reporting Lab, 'Integrated Reporting Trends Supporting Sustainable Growth in Japan 2023'.

https://www.edge-intl.co.jp/wp-content/themes/edge-intl/assets/pdf/01_reserch/02/list2023_J.pdf

Edge International, 'Integrated Report 2022 Survey - Materiality'.

https://www.edge-intl.co.jp/wp-content/themes/edge-intl/assets/pdf/01_reserch/03/s2022_05.pdf

Edge International, Creating Corporate Value through Integrated Reporting - The State of Integrated Reporting in Japan 2023.

https://www.edge-intl.co.jp/integratedreporting2023/

FSA, 'Good Practices for Disclosure of Descriptive Information 2023'.

https://www.fsa.go.jp/news/r5/singi/20231227/01.pdf

Tokyo Stock Exchange, 'Results of a Survey of Foreign Investors on English Disclosure (Summary Version)'.

https://www.jpx.co.jp/equities/listed-co/disclosure-gate/survey-reports/nlsgeu000005qpys-att/jr4eth00000015wg.pdf

Tokyo Stock Exchange, 'English Disclosure Implementation Survey Aggregate Report'.

https://www.jpx.co.jp/equities/listed-co/disclosure-gate/survey-reports/nlsgeu000005qpys-att/bkk2ed0000006oi6.pdf

*Related page*.

Report list : Regulations/standards

https://aiesg.co.jp/report_tag/基準-規制/

[Press release] aiESG launches 'aiESG for IR', an integrated report evaluation service using generative AI.

~ Scoring consistency between integrated reporting and global ESG requirements ~.

https://aiesg.co.jp/news/aiesg-for-ir/

[Commentary] Alphabet soup.

〜˜ Turbulence and convergence of sustainability standards ˜.

https://aiesg.co.jp/report/2301226_alphabet-soup/

What is materiality in sustainability reporting?

https://aiesg.co.jp/report/240201_materiality/